A Surge in Drydocking (Vol. 2)

Nov. 6, 2020

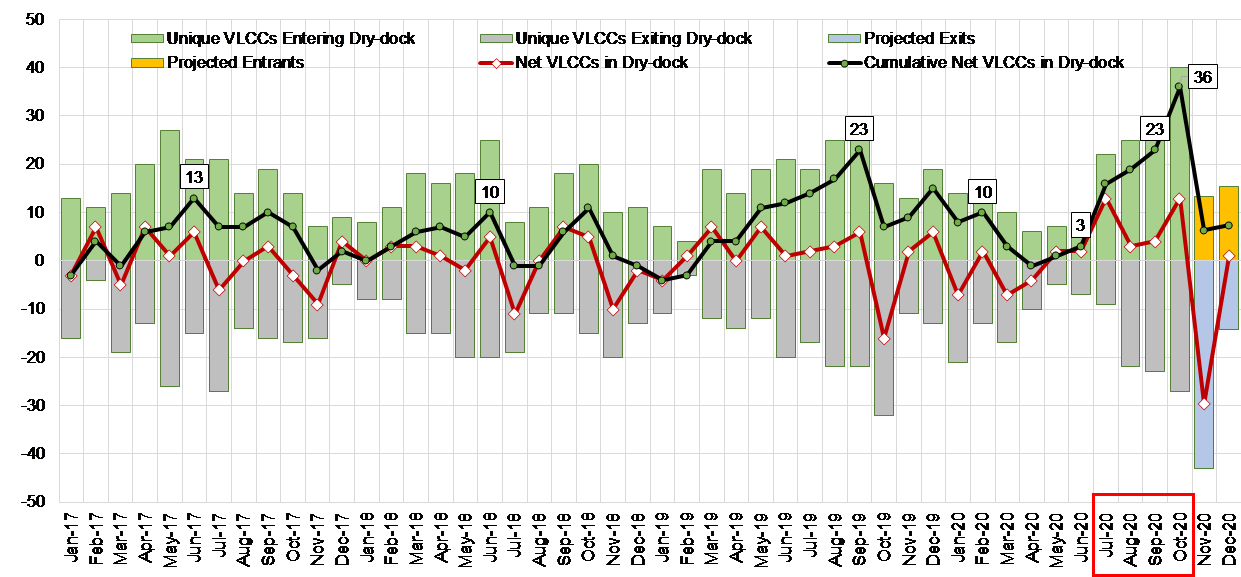

One of the main topics of the weekly highlight for the previous month is coming back in the spotlight. VLCC drydocking activity in October surpassed even our previously elevated expectation, recording the highest level (40) in recent times. This did not come as a surprise since we have already discussed how very few ships went in for drydocking during the first half of the year amid a pandemic and very high freight rates. Despite our anticipation though, the numbers we saw for October are nothing short of extraordinary.

According to the latest available data, 40 unique VLCCs have entered drydock in October, bringing the net cumulative total to 36 vessels (Figure 1). Comparatively, 27 unique tankers entered drydock in September, 25 in August and 22 in July of this year. If we look at the previous year’s peak of 23 net VLCCs in drydock in September, which was caused by a flurry of scrubber installations in anticipation of the IMO 2020 bunker fuel regulations, we can see that right now we have 13 more supertankers out of the trading fleet.

With these numbers, it would be fair to expect some support in freight rates. The absence of that shows just how much the market is oversupplied. However, the absence of upward mobility in tanker rates doesn’t mean that the increased number of ships off trading does not have an impact. On the contrary, we believe that this is one of the reasons that tanker rates have not completely cratered.

We believe that tanker owners understand these dynamics and they have chosen to time these activities accordingly. Despite the depressed markets, some owners expect that the winter season (Nov.-Dec.) will see increasing activity, which may result in a marked pickup in rates; we tend to disagree with this notion. However, we do agree that the opportunity cost for owners at present is very low, making sense to bring forward dry-docking, whether it is for regular surveys or for scrubber installation. On the topic of scrubbers, and slightly off-topic from this weekly highlight, we see the potential for HSFO and VLSFO to price at near parity in the short-term. More on this subject next week.

Figure 1 – VLCC Drydocking Activity

Source: McQuilling Services

Comments

You need to login to comment.