A Year-End Review

Dec. 24, 2020

As the tumultuous 2020 comes to a close, we wanted to take this opportunity to write a short review of the events that left their mark on the markets, keeping the focus on oil supply and demand fundamentals and their influence on the as Crude/DPP and CPP tanker sectors.

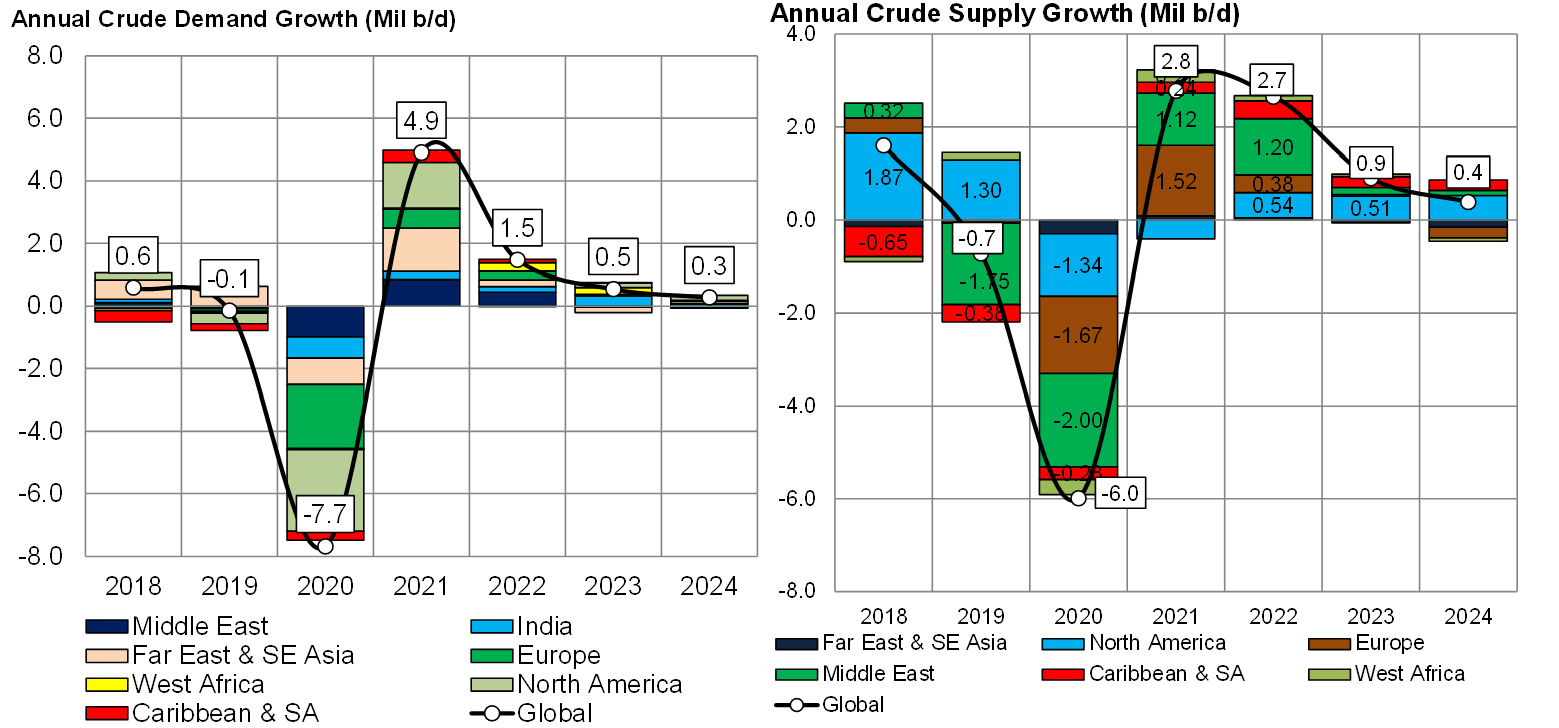

In terms of oil supply & demand, the numbers have in-fact created some deep valleys this year, with a hopeful slingshot reversal in 2021. The coronavirus pandemic kept people in their homes, and crude oil as well as its products such transportation fuels started filling up storage tanks instead of cars or airplanes. OPEC and its allies engaged in disagreements that became a short-lived price war, something that flooded the markets with even more oil. A month later, perhaps realizing the demand situation was far worse than anyone could have imagined, they came together again to decide on the deepest production cuts in history. With the cuts in place, demand started picking up as economies started reopening in early spring in Asia and late spring in the West. By 4Q 2020, a second wave of infections brought back restrictions although sentiment is somewhat balance, dare we say, positive that the worst may be behind us and 2021 will bring back “normal” markets.

In the DPP sector the dominant story was floating storage. As oil prices crashed because of the OPEC-Russia price war and COVID demand disruptions, traders found an opportunity to fill up land-based and floating storage. For April and May we experienced the most volatile freight market in history, one that brought earnings for VLCCs close to US $300,000/day and the number of VLCCs storing crude oil to over 95. That was about it as far as excitement goes. Once inventories, floating or otherwise, were full, rates began to drop seemingly without stop, reaching or falling below OPEX levels in some cases. There has simply been no growth in transportation demand, in fact we are still well below tanker demand levels pre-COVID, and the bottom in rates supported only by a record-braking number of ships we saw in drydock in recent months.

Floating storage was the story that affected the rates in the CPP sector as well. While not as pronounced as with dirty tankers, demand to store clean products soared and with it, clean tanker freight rates. The downward path was more or less similar, especially in the West where human movement barely picked up before new infections and new restrictions. Despite all that, we did identify some “winners”, with the top one being the West to East naphtha trade. As world oil production came down, so it did for LPGs, a regular feedstock for refineries, especially in East. The more expensive LPG was more readily replaced with naphtha, a product abundant (in terms of balances) in the West and we kept seeing increased fixtures throughout the year.

Figure 1 – Annual Crude Demand and Supply Growth

Source: JBC Energy, McQuilling Services

Comments

You need to login to comment.