Caribbean Fundamentals Pressure Demand

Feb. 27, 2018

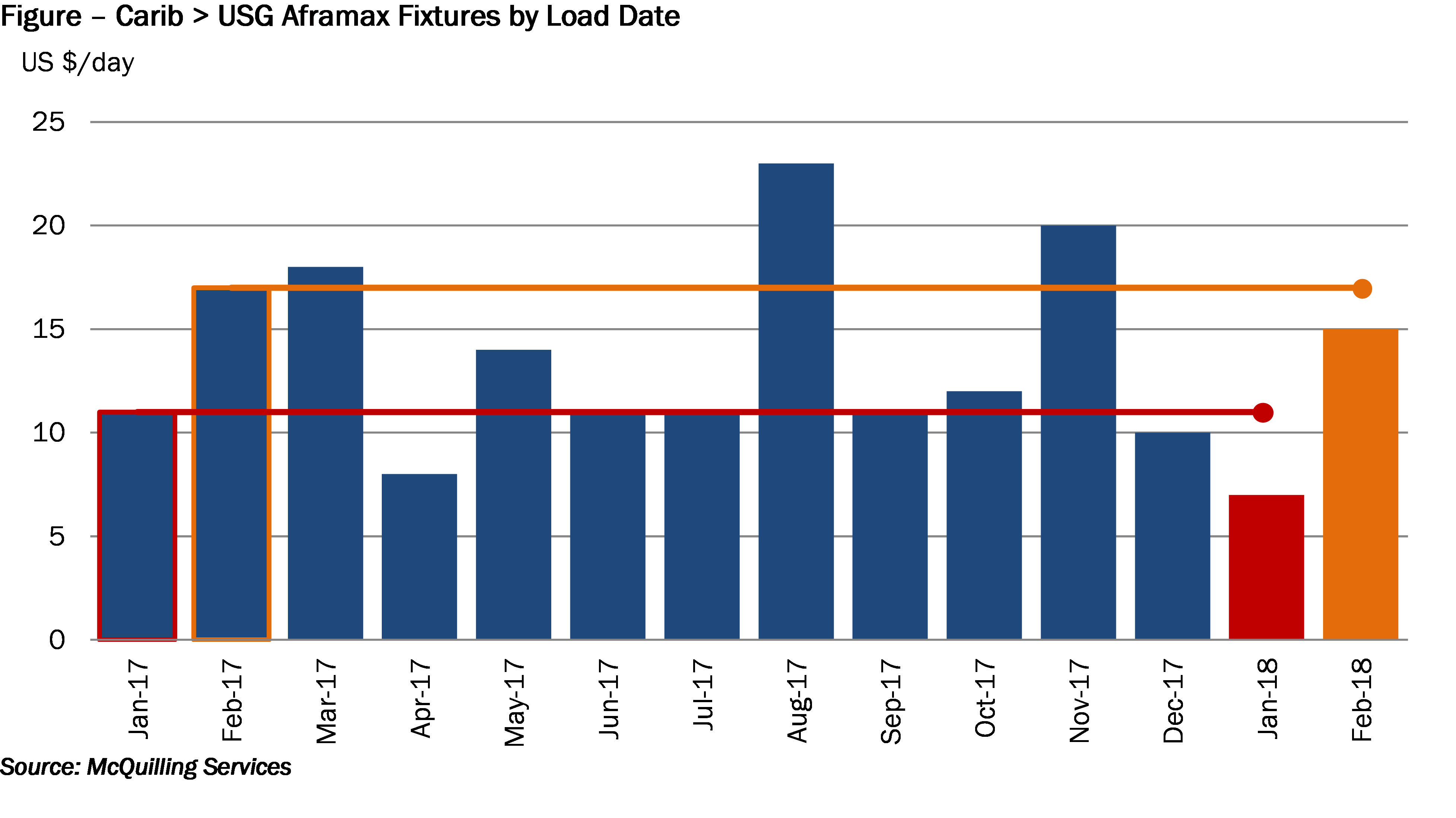

In our 2018-2022 Tanker Market Outlook, we explained our future expectations of weaker Aframax demand along the Caribbean > US Gulf trade, which accounts for roughly 4.7% of total sector ton-mile demand. In January, we stated “On the other side of the Atlantic, the benchmark Caribbean > US Gulf trade collapsed by 11.3% in 2017 as a result of lower Venezuelan exports at the expense of longer-haul trades. In 2017, Venezuela’s crude only exports to the US are estimated total 25.5 million tons. Slowing Venezuelan production is expected in the medium term with as much as 300,000 b/d at risk, coupled with higher US and Canadian output is projected to negatively impact this trade in the five year outlook. We forecast a 2.6% annualized decline through 2022.”

We are now observing this trend in the market as year-to-date fixing activity shows a 21% decline in volumes year-on-year along this trade (Figure). US crude production has increased to a height of 10.25 million b/d, while higher output has also been observed in Canada, both of which are reducing the need for import volumes into the US Gulf. According to JBC Energy, Venezuelan crude output is over the first two months of 2018 is estimated around 1.6 million b/d, roughly 370,000 b/d lower year-on-year. This trend is likely to persist through the remainder of the year, on the basis of lower Aframax demand in the region and we expect TD9 to average around the WS 107 level this year. Year-to-date, spot rates on this trade have averaged WS 104 with recent short-term support stemming from persistent port delays in the US Gulf due to weather.

Comments

You need to login to comment.