Conflict Shakes Middle East Exports

July 26, 2018

Saudi Arabia has announced a temporary halt on oil shipments via Bab el-Maneb with immediate effect after reports of two tankers attacked by Yemen’s Houthi militia surfaced mid-week. It’s been reported that the two vessels were owned by Bahri (Saudi National Shipping Co.) and that no injuries or spills resulted from the incident. Bab el Maneb separates Yemen and East Africa and is one of the largest shipping channels in the world, allowing Arabian Gulf petroleum exporters access to the Suez Canal and in turn the European market. A halt of flows through this channel is sure to leave significant impacts on the shipping markets as some other Middle East nations have expressed concern with Kuwait indicating a potential halt in flows, while Iraq will continue exports as normal, given it sells on a free-on-board basis passing the transportation risk onto the buyer.

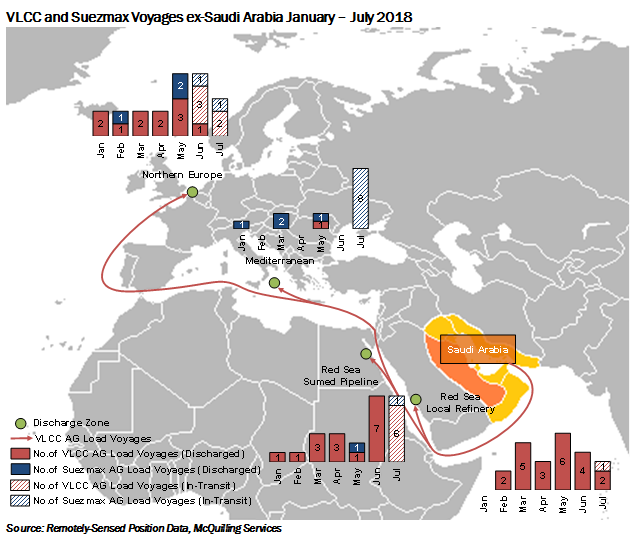

Further analysis of our remotely sensed vessel position data tells us that 40 VLCCs have completed voyages from the Arabian Gulf to Northern Europe and the Mediterranean since the beginning of 2018, while 14 additional vessels are in transit on this same route. Of these 54 ships, 17 were loaded in Saudi Arabia indicated by the voyage map below. Additionally, 73 VLCCs stemming from the Arabian Gulf have discharged or are currently set to discharge in the Red Sea, with the a majority of these volumes likely bound for Ain Sukhna, the beginning of the Sumed pipeline, which connects the Red Sea and Mediterranean. The disruption of Bab el-Maneb is likely to negatively impact Middle East volumes into the European market, which in our view will result a small rise in volumes sent around the Cape of Good Hope. While this may result in higher ton-miles for specific voyages, we are reluctant to say the rise will be significant as we project Arabian Gulf producers to focus higher crude exports to the East, leaving European refiners to source barrels elsewhere. Given the current narrowing of the Brent-WTI crude differential to an average US $3.06/bbl this month has pressured US crude volumes to the East, we see a potential for US crude to serve the European market, in place of Middle East crude.

Another potential outcome is increased volumes along the Petroline pipeline, which runs across Saudi Arabia connecting oilfields in Abqaiq to the Red Sea port of Yanbu, boasting a total capacity to transport 5.0 million b/d of crude or roughly 50% of the nation’s total production. However, the full capacity is not in use today and it is our understanding that the infrastructure was constructed as an “insurance policy” in the event of a closure of the Strait of Hormuz. It is currently unclear if Saudi Arabia will utilize this pipeline to bypass Bab el-Maneb and send crude through the Sumed pipeline to the European market; however, this would likely mitigate the expectation of negative pressure on demand for tankers loading at the Mediterranean port of Sidi Kerir. We must also keep in mind that Iran recently indicated it can disrupt Arabian Gulf exports via the Strait of Hormuz, further supporting the notion that Saudi Arabia may look towards land-based infrastructure as a solution.

We are certain to see volatility in the tanker freight markets for the foreseeable future as trade flows shift within the largest crude export region of the world. Volumes to the East are likely to remain in place or potentially rise, while exports to the West will have to take the longer voyage or refiners will source from alternative regions. Additionally, support for volatility will also stem from the supply side as internationally flagged fleets will likely be the preference for exporters in an effort to protect state-controlled tonnage.

Comments

You need to login to comment.