Demand Revisions: Will They Support a Crude Tanker Recovery?

Nov. 12, 2021

Revisions on global supply, demand and the resulting balance have been the norm lately given the uncertainties brought by the ongoing pandemic and pockets of resurging infections (especially in Europe), the global supply chain bottlenecks as well as inflationary pressures and the possible fiscal responses from governments and central banks.

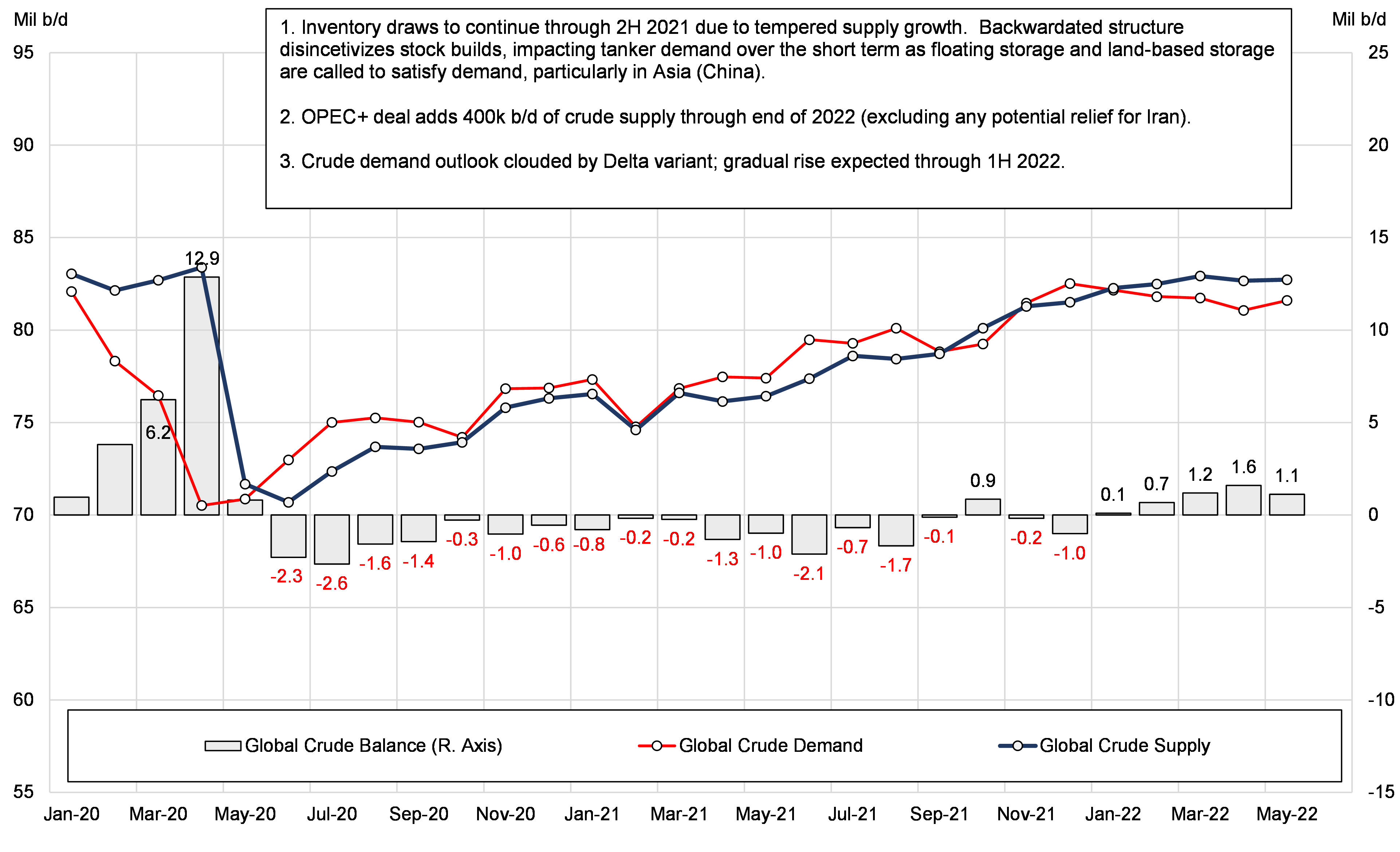

OPEC and allies decided to stick to the 400,000 b/d monthly supply increase in their November meeting, while a few days later the organization revised its 2021 oil demand forecast down by 160,000 b/d to a total of 5.7 million b/d. Despite that, JBC Energy forecast global crude oil demand to outpace supply slightly, by 179,000 b/d, compared to the 861,000 b/d of surplus the previous month.

Going forward, the data reveals a growing crude balance deficit of about 1.0 million b/d in December as a result of winter demand, a component of which is the “gas to oil” switch for power generation, especially if gas prices remain elevated over the balance of Q4 and Q1 of next year. Inventory drawdowns, both land-based and floating are likely to be further incentivized during this period and we expect tonnage that is performing the latter to continue being released in the trading fleet, maintaining an element of pressure on the prevailing freight rate structure. In fact, our updated VLCC supply/demand models point to a disappointingly flat freight market in December m-o-m.

As we enter 2022, Q1 runs the risk of less global mobility (especially given the uncertainties discussed) and decreasing crude demand in the refinery level, while at the same time OPEC+ is expected to keep adding production, supported further by the gradual increase in US shale oil production. The resulting crude surplus, growing from 105,000 b/d in January to 1.2 million b/d in March (Figure 1) could help ease prices and in turn incentivize additional buying from refineries, an overall positive for crude oil tankers. Although uncertainty and vessel supply side risks remain with very low demolitions so far this year, the road to a tanker recovery could start as soon as Q2 2022, especially as it connects with refiners increasing crude purchases in anticipation of summer driving season. However, demand alone will not be enough to return owners to all-in break-even levels; considering the heavy orderbook schedule for next year. In short, the crude tanker market needs deletions; without them, the road to recovery will continue to get longer.

Figure 1 – Global Crude Oil Supply, Demand and Balance

Source: McQuilling Services, JBC Energy

Comments

You need to login to comment.