Does Floating Storage Make Sense

March 20, 2020

Just a few days ago, Saudi Arabia’s fallout with Russia had the former increasing oil production to over 12 million b/d for April and discounting its official selling price (OSP) for crude in order to gain market share. As a result, oil prices retreated to levels not seen in many years and the markets started showing a contango structure. The promise of a cheap current contract and a higher future price create the ideal scenario for someone who has the capacity to store product for future or sell it later.

Floating storage activity could be categorized into two groups – operational and commercial. Operational floating storage appears when the onshore storage reached or near its capacity. For example, we observed increasing FS activities in South East Asia prior to 2020, when the onshore storage units are preparing to switch from HSFO to VLSFO storage. At that time, VLCCs were deployed to ensure a smooth switchover in one of the world’s busiest bunkering hubs. Compared to operational floating storage, the commercial floating storage would happen when the contango structure supports this activity – in short word, “when money makes sense”. To determine whether the latter make sense in the current market, traders/charterers would not only take the crude/product M0/M3 or M0/M6 spread into consideration, but also the short-term time charter rates.

Combining all the above, we see that the current TC rates do not yet support such action although there is potential for it if rates keep falling. In the table below, we show the max TC Rates required to breakeven on a commercial floating storage scenario, using crude pricing data from this week. Anything below the “Max TC Rate” can, in theory, make commercial sense.

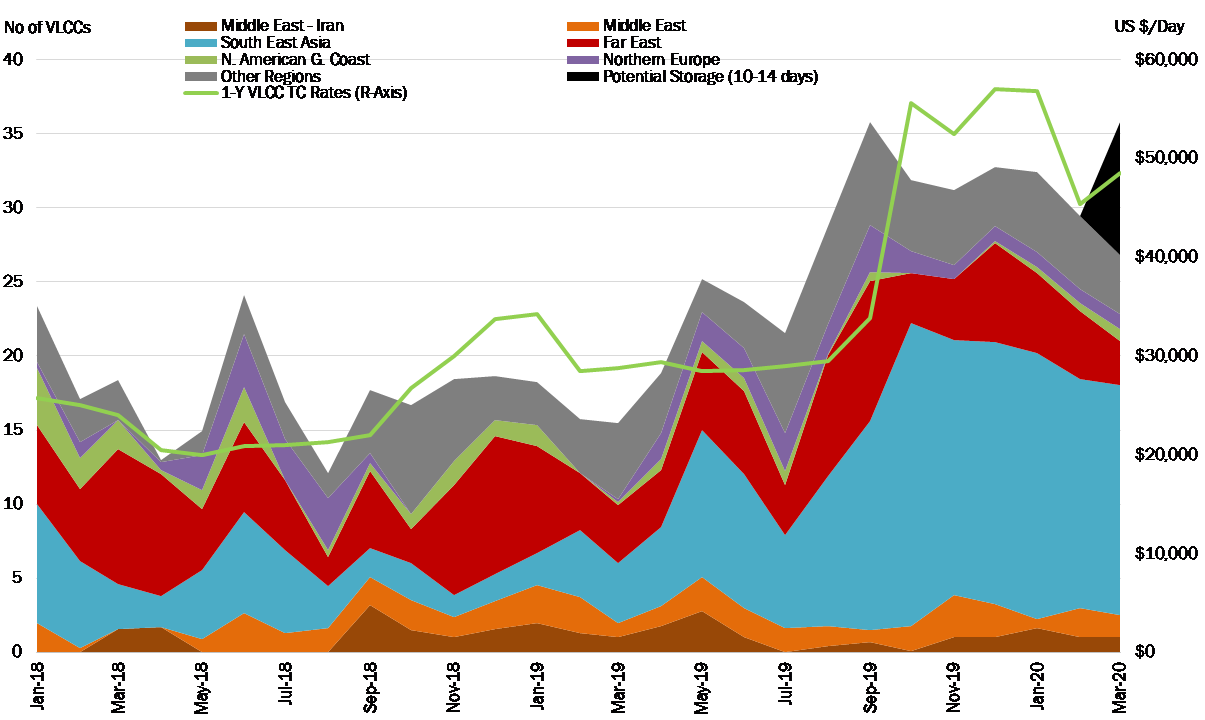

As we notice the freight rates for the tanker markets falling in the past couple of days, lower TC rates could potentially raise the number of tankers devoted to floating storage to levels seen during the preparation for the new IMO regulations in this past September of 2019 (Figure 1).

Figure 1 – Monthly Average Floating Storage – Jan 2018 – Mar 2020

Source: McQuilling Services

Comments

You need to login to comment.