Dubai Weakness Promotes AG Exports

March 15, 2018

In McQuilling Services’ March Short-Term Outlook, we expressed our expectation of higher crude demand out of the Arabian Gulf in the near term due to recent weakness in Dubai crude pricing. In our report, we note the expansion of the Brent-Dubai crude differential, averaging about US $3.04/bbl through the first half of March, up from US $2.61/bbl in February. The growing presence of US crude flows to Asia is likely a supportive factor as we observed February crude exports average roughly 1.5 million b/d, according to preliminary estimates by the US EIA, which compares to 1.1 million b/d over the same month of 2017. Additional pressure is likely stemming from lower domestic demand in the Arabian Gulf with refinery maintenance estimated at an average of 810,000 b/d over March/April. As a result, JBC Energy projects the balance of Middle East crude supply to rise above 20,000 b/d placing additional pressure on Dubai–linked grades and, in our view providing more incentive for Asian refiners to source this crude.

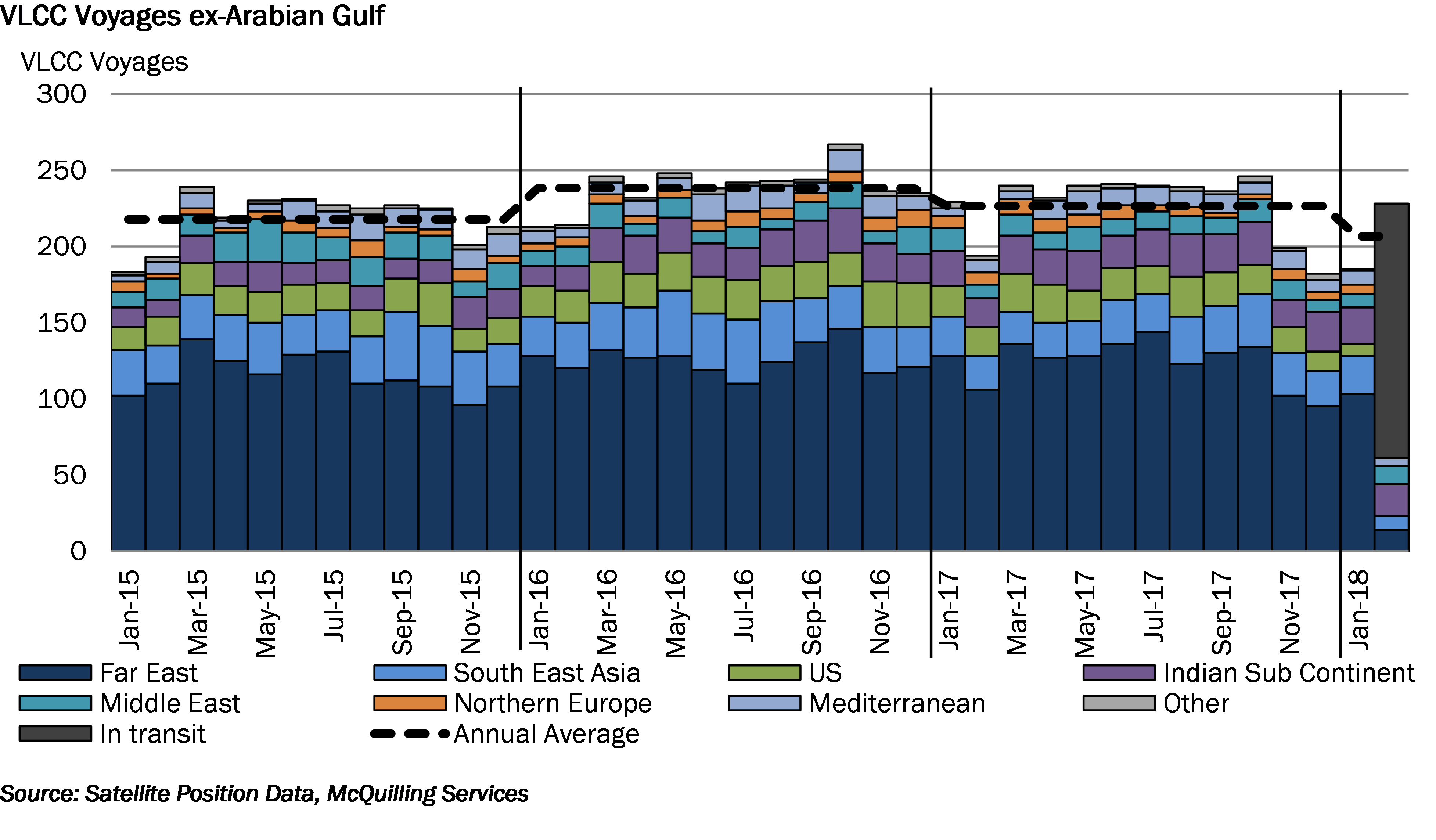

We note a recent increase in VLCC loadings out of the Arabian Gulf/Red Sea region, which reached 228 loadings in February, a rise of 17% year-on-year and 23% month-on-month (Figure). Tanker owners in the region will likely see some short-term support from the demand side of the equation; however, we must note that this may not come to fruition in the form of higher freight rates as the continued oversupply of tonnage will likely keep a cap on any major rate gains.

Comments

You need to login to comment.