Highlighting Expectations for VLCC Demand

May 22, 2020

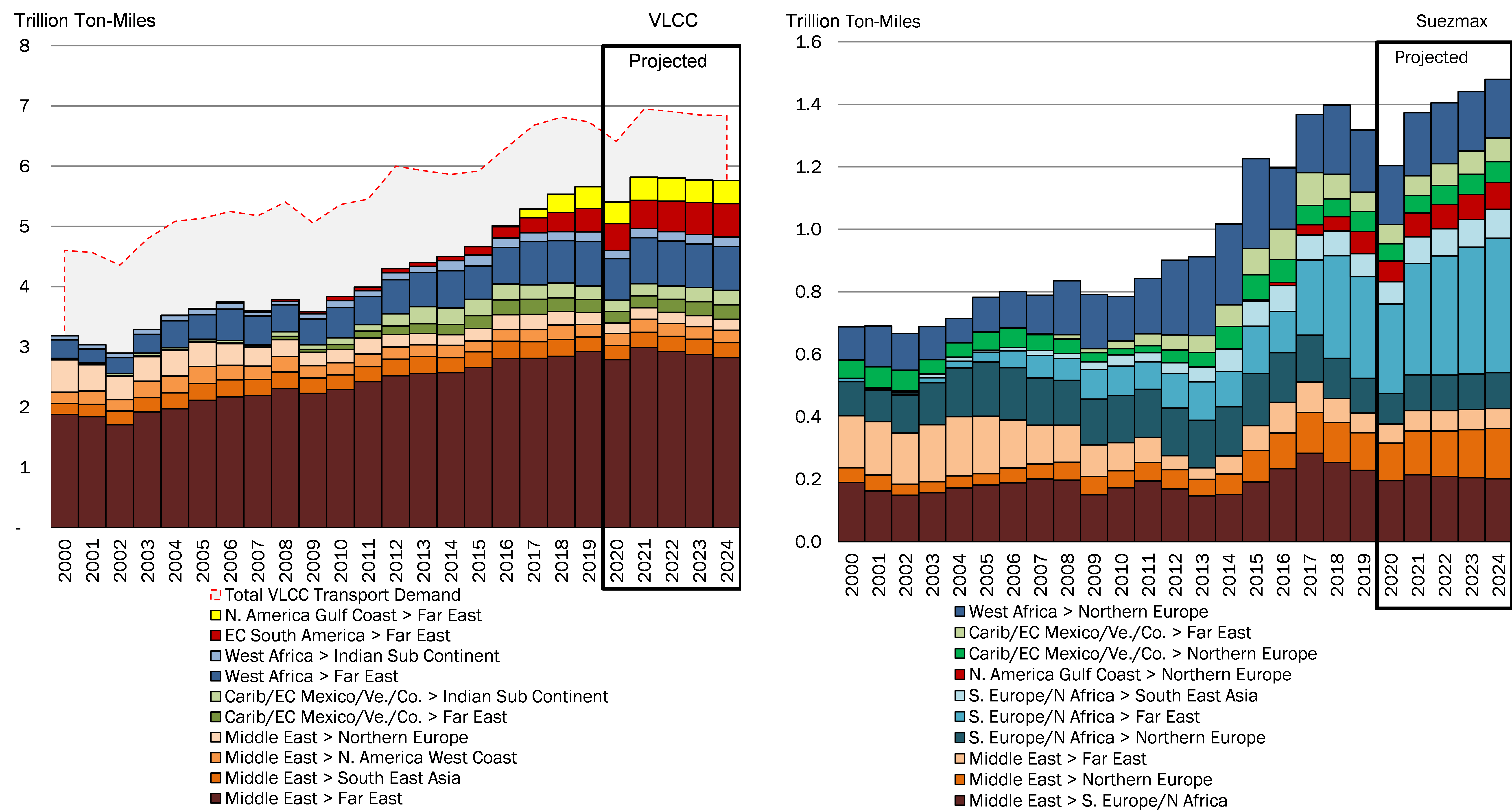

The extraordinary times we are finding ourselves in have led analysts to revising projections and conclusions that were produced months, sometimes even only weeks prior. Similarly, projections on tanker demand for DPP cargos do not follow any kind of “normal” based on previous years and a world without a pandemic. Despite that, a few fundamental things remain the same. Two-thirds of tanker demand is still generated by VLCC tankers and remain the focus of our analysis along with crude balances, which drive that demand.

Overall, our analysis of tanker demand projects a drop of 4.8% in 2020 compared to the previous year. This is fundamentally attributed to a largely reduced demand for crude due to the pandemic. Looking at the Middle East to Far East trade, responsible for almost 50% of VLCC demand, we too expect it to drop a significant 5.3% in 2020 as compared to 2019 (Figure 1).

To understand the expected drop, we need to look at the projected global crude balance. Of course, in the past few months this has become somewhat complicated to explain. The flood of oil in March and April created a serious surplus, which in turn created a short-lived frenzy in trades. However, due to the lack of end user demand, almost all this oil went to storage, either on land or floating. The quick policy reversal of OPEC and its allies resulted in some of the deepest production cuts in history beginning in May. These cuts will quickly create a deficit in crude but in the meantime, refiners globally have ample inventories to tap into, thus reducing the need to bring in more oil in ships, even when economies return to normal.

We have previously discussed that Middle East producers would likely focus on retaining market share in the East and this appears to largely remain the case for 2020. The brief disruption stemming from the collapse of oil prices and aggressive production in the region will most likely contribute in seeing a handful of additional VLCC voyages to the US Gulf, but with the cuts working, this is likely the exception that proves the general trend of the weak Middle East crude volumes to the West. Our projections show approximately 75 VLCC voyages to the USG for 2020 as compared to 46 for 2019. Through May 7, these voyages (VLCC AG>US Gulf) reached 26.

Figure 1 – Middle East Loaded VLCC and Suezmax Voyages

Source: McQuilling Services

Comments

You need to login to comment.