LPG Supply/Demand Highlights

Oct. 15, 2021

LPG demand has been making headlines recently, mainly due to the recent pricing volatility in the Asian markets, but also in the West of Suez (Europe/US). Asian markets are currently increasing LPG stocks in anticipation of winter heating demand, tightening the market as petrochemical facilities ramp-up their feedstock requirements amid an improving global economy. One result of this pricing strength for LPG was observed in August/September when demand shifted to naphtha as a feedstock, supporting LR volumes and freight rates on the benchmark TC1 AG/Japan trade. This week, reports by Platts and other sources pointed to a reversal of propane prices in Asia, which may shift petrochemical plant feedstock preferences away from naphtha in the short term.

The prospects of LPG are bright and has prompted us to begin developing fundamental views on the commodity, synthesized with vessel supply projections to project directional moves in rates. In terms of LPG supply, one of the largest suppliers is the US, and US LPG production is closely related to that of shale oil, but also natural gas. On an average basis, we project that US LPG length will trend lower in 2022 due to the discipline of US shale producers, while demand remain relatively supported, particularly over the winter markets. This has the potential to temper US LPG exports during this period.

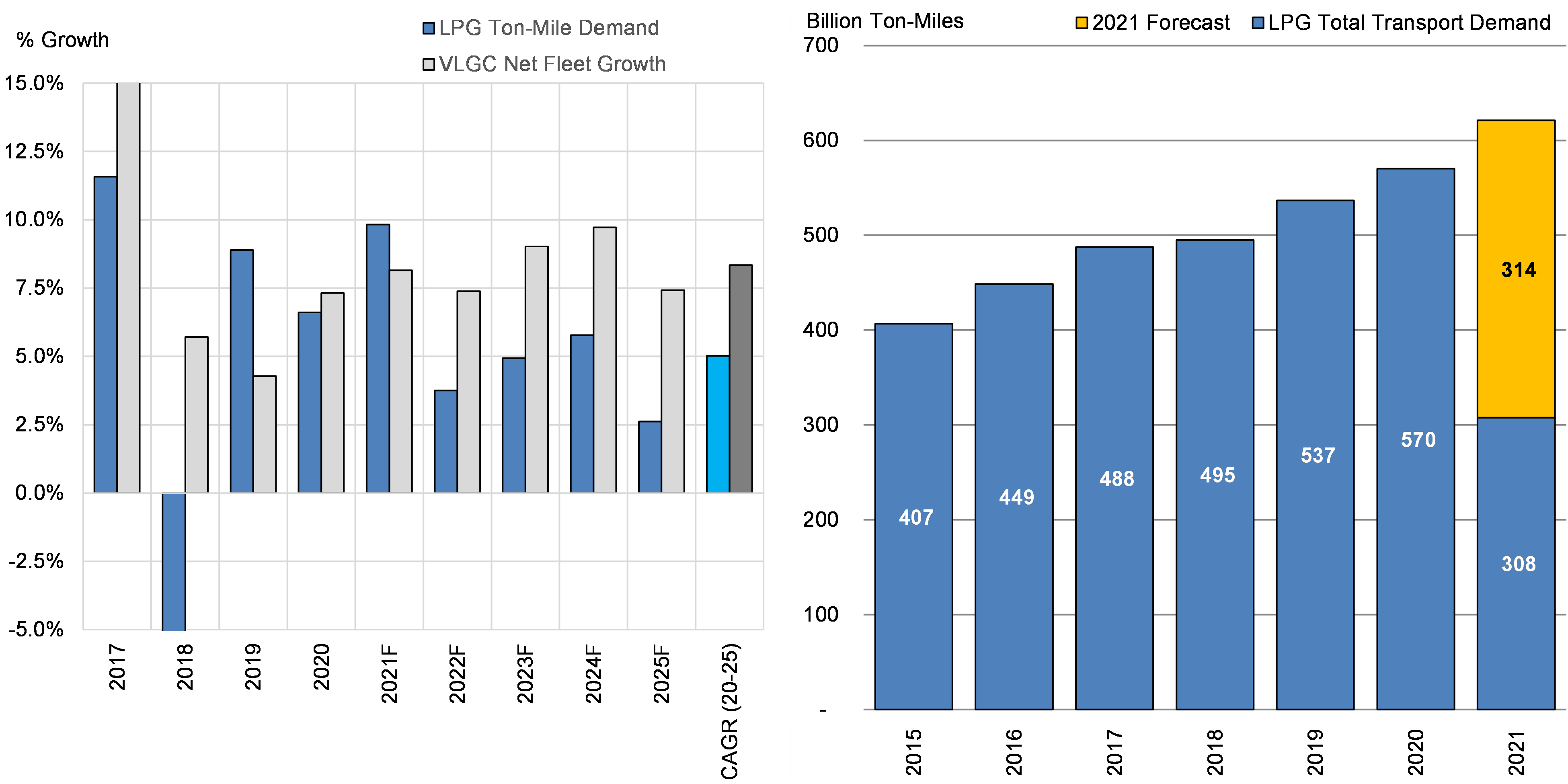

On a global basis, our proprietary calculations of ton-mile demand reveal an increasing trend for global LPG transport demand to 622 billion ton-miles for 2021 (Figure 1). Ton-mile demand originating from the US Gulf region has been the primary contributor to VLGC demand over the last few years, although our models point to a more modest growth next year, before accelerating in 2023. The Middle East is also expected to add LPG length through 2025 although exports are likely to head to the Indian subcontinent instead of the Far East, resulting in less ton-miles.

For the supply side variable, we project approximately 100 VLGCs to be delivered between 2021-2023, which combined with low anticipated deletions (historical avg. age of VLGC Deletions = 30) is projected to place pressure on the freight market as supply growth outpaces gains in ton-mile demand over the forecast period (Figure 1).

McQuilling Services is pleased to announce that in Q1 2022, we will publish our inaugural LPG Carrier Market Outlook report, following the same structure as our market leading Tanker Market Outlook publication.

Figure 1 – LPG Ton-Mile Demand and Net Fleet Growth (Left Graph) & LPG Total Transport Demand (Right Graph)

Source: McQuilling Services

Comments

You need to login to comment.