Mexico’s Clean Imports on the Rise

April 10, 2018

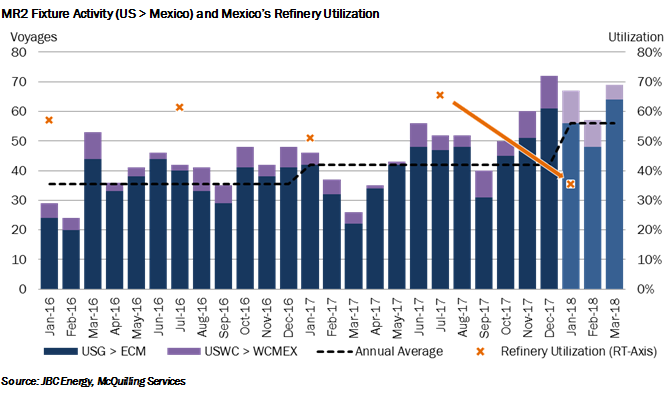

The Caribbean refining sector remains under pressure with recent market reports indicating that utilization declines have exceeded the typical seasonal decline for this period. JBC Energy estimates that Mexican refinery utilization dipped to a low of 33% in February, from a high of 65% in July 2017, amid lower crude throughputs at six Pemex refineries (Figure, orange arrow). Levels at these refineries averaged less than 550,000 b/d in February, down about 385,000 b/d versus the same period in 2017, when utilization was around 51% of capacity. Even though the Madero and Minatitlan refineries returned online late February, the Santa Cruz and Tula refineries have struggled to ramp up intake. JBC Energy has since lowered its expectations for growth in this sector, previously forecasting Mexico’s refinery intake to average 750,000 b/d through the first half of this year and now revising this figure to 630,000 b/d, leading to a projected 11% decline year-on-year for all of 2018. Gasoline production plummeted 140,000 b/d year-on-year, to average 165,000 b/d in February stimulating more import activity to meet regional demand.

The US has stepped in to meet these requirements with activity along the USG>ECM route surging since the end of 2017. Utilizing McQuilling’s proprietary fixture database, we count an average of 56 MR2 voyages per month along this route, through the first quarter of 2018, which compares to 32 over the same period of 2016 (Figure). We have also witnessed more trading from the US West Coast to the West Coast of Mexico in comparison to last year. Taking a look at our weekly estimates for MR2 positions in the US Gulf, we note a 2.7% decline in average number of positions over the first quarter of this year versus last, which may be a symptom of increased trading activity between the US and Mexico. The USG > Caribbean (Pozos) MR2 trade route has averaged around US $460,000 through the first three months of the year, a 4.5% rise from the same period of 2017 and we expect this trade to find further support through the second half of the year in concert with the overall rebalancing of the clean tanker market.

Comments

You need to login to comment.