Mid-Year DPP Earnings Review

Aug. 8, 2020

As we are over the mid-year mark in a year when not many things have been “normal”, we decided to look back and examine the main events that have shaped earnings in the DPP tanker sectors to date. The beginning of August signifies the end of the “chapters” of additional floating storage as well as the deepest OPEC cuts in history.

The two main events affecting the tanker market were the global coronavirus pandemic that led to a destruction of oil demand and the short-lived price war initiated by Saudi Arabia in early March. Despite the lack of demand, almost all tanker sectors entered a rate frenzy after the latter due to the very cheap oil, the contango market and the availability (at that time) of storage space.

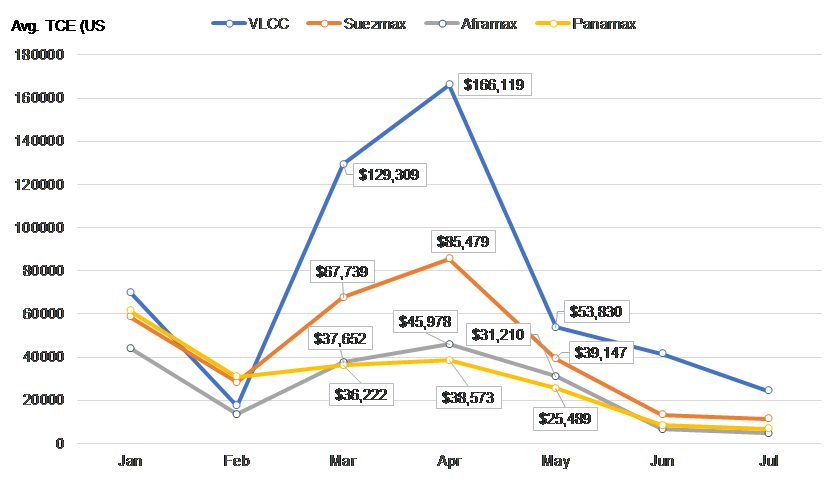

The main story in the VLCC sector was the floating storage of crude oil. The opportunity to buy low and -potentially- sell high in the future had traders scrambling to find suitable ships to store as much oil as possible. As ships were taken off the market and tanker demand increased, earnings skyrocketed almost nine times over from the lows of February to the peak in April (Figure 1).

The Libyan civil war and subsequent halt of most oil production and exports in the country since late January was the event that further shaped the DPP sector. The Mediterranean trade has all but ceased for the Suezmax sector. However, Suezmaxes traditionally fill in when VLCCs can’t be found, both in spot trading and floating storage, making average earnings show a very strong increase as well.

Looking at the Aframax sector, while earnings increased from February to April, they barely surpassed January levels at the peak. One of the reasons for that was the number of LR2 tankers pivoting to dirty trading as owners looked to capitalize on the vast opportunities during March-April, thus increasing Aframax supply.

In terms of earnings, the Panamax sector has been the most “stable” within the global developments. In fact, Panamax TCEs were stronger in January than April (Figure 1). In the very low demand environment, the sector was not used for floating storage and neither did it replace many Aframaxes given the influx of LR2s in the latter sector.

With inventories filled and demand still struggling to pick up amid a recurrence of coronavirus infections, we are currently in a low demand environment for tankers. Looking at the second half of 2020, we expect the trend to continue with ship supply getting longer as tankers exit floating storage. Barring any more unexpected events (e.g. Venezuela sanctions), it is likely that the weak earnings period will last well into 2021.

Figure 1 – TCE Development per Sector – Jan to Jul 2020

Source: McQuilling Services

Comments

You need to login to comment.