Owners Continue to Order

Aug. 22, 2017

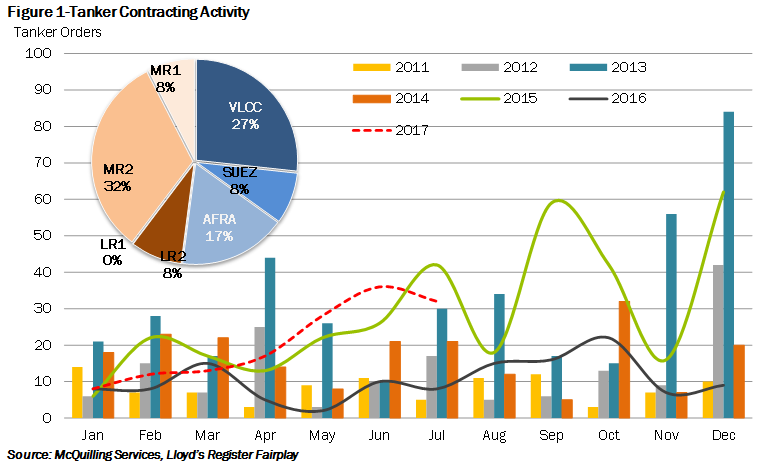

There have been 146 tanker orders placed through July, compared to just 56 during the same time period last year. The bulk of these orders have stemmed from the VLCC and MR2 classes as 39 and 47 firm orders have been placed, respectively (Figure 1). Maran Tankers placed a firm order for seven VLCCs at Daewoo this year, while BW/DHT has collectively placed six at Samsung and Hyundai Heavy Industries.

For DPP tankers, trailing the VLCC sector, 12 Suezmaxes and 25 uncoated Aframaxes have been ordered through the end of July, a dramatic increase from the 11 Aframaxes ordered last year, but broadly in-line on the Suezmax side. The resilience of newbuilding contracts has pushed us to adjust our vessel delivery schedule for the outer years of our forecast and, in turn, lowered our freight rate expectations.

In the clean tanker segment, newbuilding ordering has reached 70 vessels this year, four and 48 more than the same period in 2016. We have counted 47 MR2 tanker orders in 2017, not including any chemical (IMO 2 designated) MR2s. In the LR tanker categories, AP Moller has been active, ordering six vessels at Dalian, while Ship Finance International preferred Daehan for its two newbuilds. In total, we count 12 LR2s and 0 LR1s ordered year-to-date.

Order a copy of McQuilling Services 2017 Mid-Year Tanker Market Update

The Mid-Year Tanker Market Outlook Update provides an outlook for spot market freight rates and TCE revenues for 19 major tanker trades, including two triangulated trades, across eight vessel classes for the second half of 2017 and the remaining four years of the forecast period to 2021. We revisit our forecasting process at the mid-year point, distilling data from the first half of the year to better understand recent market developments and expectations for the future. In our view, this process allows us to accurately adjust our forecasts and provide additional value to our clients.

Comments

You need to login to comment.