Refinery Capacity Developments & Tanker Demand Impact

Nov. 19, 2021

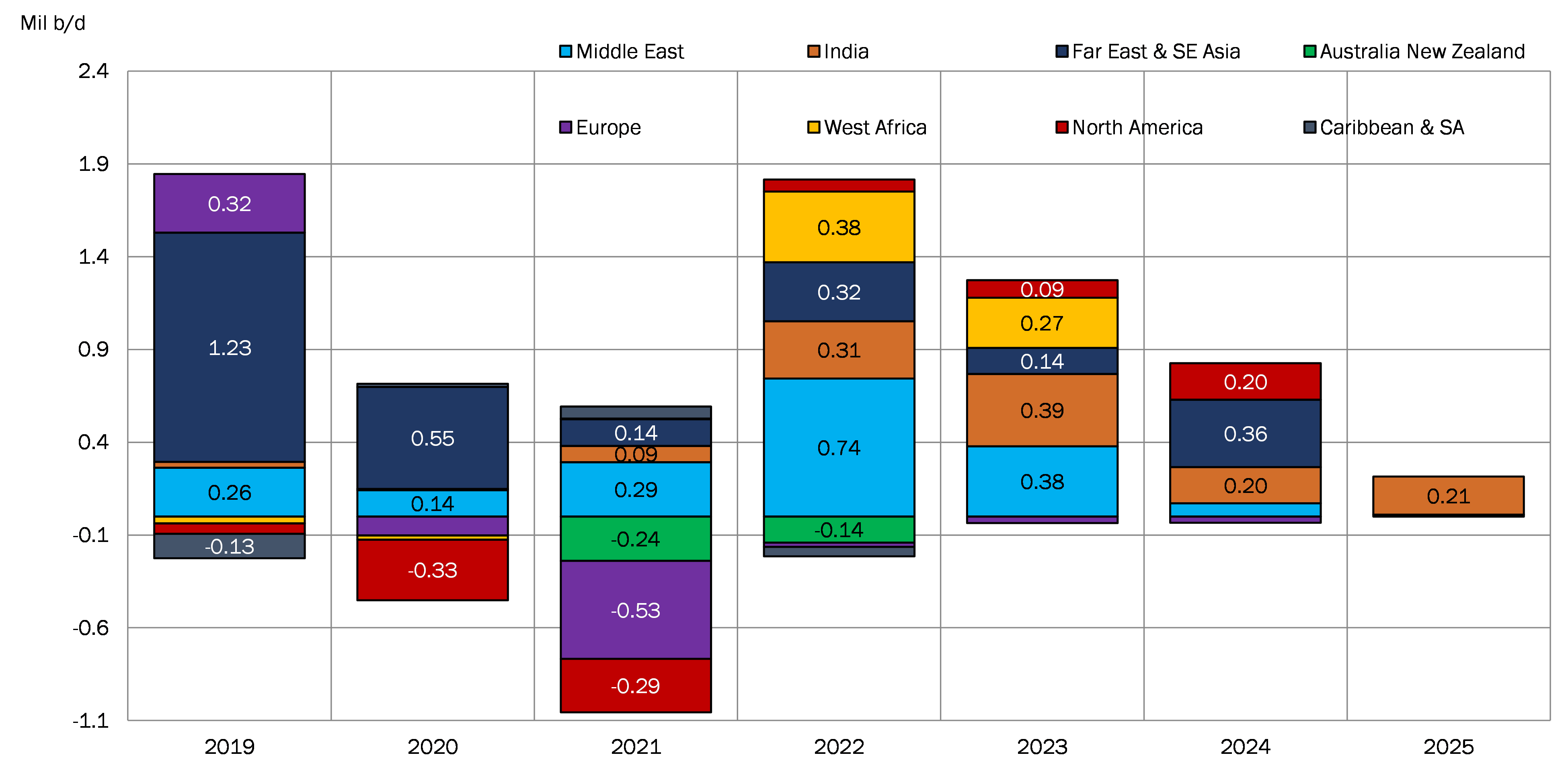

One characteristic of the current year is that global refining capacity is shrinking by close to 638,000 b/d according to the latest data from JBC Energy (Figure 1). We have observed closures and conversions increasing since 2020, with the bulk of the reductions transpiring in Northern Europe as the region is intensifying its decarbonization push and the move away from fossil fuels. A similar story is developing in North America, this time around the US West Coast where refinery consolidations and conversions to biofuels production facilities have also become prominent this year.

Going forward, we note the division between the West of Suez and East of Suez markets, with the former essentially not replacing lost capacity but rather focusing on investing in more sustainable technologies such as renewable power generation sources and cleaner fuels. A glaring exception is the Dangote refinery in West Africa which, as we have already covered in previous highlights, will likely alter the ton-mile demand for DPP and CPP tankers in the region from 2023 onward.

As local product demand grows in the East of Suez markets, so does refining capacity. Owing to the recent energy crunch in China and other Asian economies, our attention is becoming even more pronounced on developments in Far East and Southeast Asia. Through 2025, the latest data reveals that the region is projected to add close to 965,000 b/d of new processing capacity (Figure 1). Despite that, we note that demand in the area, particularly SE Asia, is likely to continue increasing at a rapid pace, outpacing product supply and creating a stable need for product imports in the region. Among those, the data shows a growing naphtha deficit (~350,000 b/d by 2025) that is likely to support LR tanker demand in the medium term, augmenting strong distillate export flows from the Middle East’s expanding refining sector.

Finally, on the DPP side, increased East of Suez capacity will continue to support crude tanker demand. The incremental addition of 400,000 b/d from OPEC+ for December is likely to be absorbed in its entirety by Asian refiners, keeping the regional balances tight as we enter 2022 (JBC Energy). Middle Eastern crudes are expected to remain prominent in the region, especially to the Indian Subcontinent where processing units are geared towards those grades and additions are forecasted to reach over 1.18 million b/d by 2025. While the volume increase is positive for crude tankers, our updated ton-mile demand models reveal decreasing mileages for Middle Eastern crudes over the medium term.

Figure 1 – Global Refining Capacity Additions

Source: McQuilling Services, JBC Energy

Comments

You need to login to comment.