Thoughts on Iran and Venezuela in the Context of a Biden Administration

Dec. 4, 2020

Beginning with Venezuela, a Biden administration could potentially be considered more “lenient”, thus opening-up a path to diplomacy rather than the heavy-handed approach from the Trump administration. But, even under ideal circumstances - Venezuelan production declines are not easily reversible after chronic under-investment, considering also that maintenance has been minimal at best over the last few years. The main importers of Venezuelan heavy, sour crude have historically been the US, China and India. These barrels would substitute other heavy sour barrels (mostly AG). With that in mind, if those three buyers were to increase, the impact is more Aframax demand from the Caribbean to the US Gulf, while reducing the already weak Arabian Gulf VLCC trade to the West (net negative). Towards the East, we would project more VLCC demand to China and India, substituting VLCC demand from the Arabian Gulf to these markets (net positive).

Switching to Iran, a Biden presidency would likely reduce the hard-line approach from the Trump administration – thereby allowing them to sell their oil freely, increasing the demand for tankers. But any such policies would also return the Iranian tanker fleet to the market, thereby increasing the supply of ships, although 50% of the Iranian VLCC fleet is likely to be underutilized due to age and vetting restrictions. Analyzing the impact on tanker demand, Iranian flows to China are about 50% of the ton miles of US barrels to the Far East – a negative impact on tanker utilization. In addition to Asia, it would be likely that Iranian crude oil would be shipped to Mediterranean refineries as per historical trend volumes, supporting Suezmax demand. This would likely come at the expense of Iraqi Heavy, but also Urals to some extent, putting further pressure on regional crude pricing dynamics. One consequence of the increasing supply of crude oil in Europe would be a very difficult arbitrage movement from the US Gulf, in the context of a tighter crude balance in the US as Iranian (and Venezuelan) supply increases will likely lengthen the overall crude balance and pressure prices.

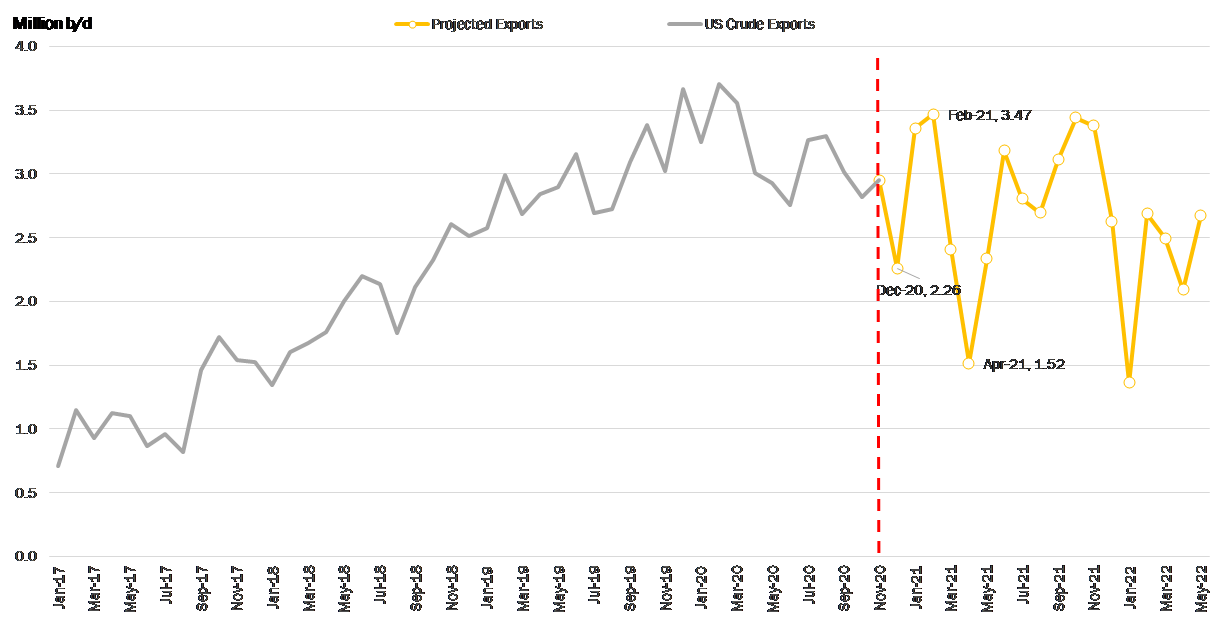

Overall, a more lenient approach to Venezuela and Iran from the Biden Presidency, would likely coincide with a shift to a more “green” energy mix in the United States and questioning the overall growth prospects of the shale industry. However, even without the aforementioned policy approach, we project a weaker US crude export cycle on the horizon due to tightening balances along with increasing supply from OPEC+ countries, albeit slightly more delayed than originally thought (Figure 1).

Figure 1 –Historical and Projected US Crude Exports

Source: IEA, JBC Energy, McQuilling Services

Comments

You need to login to comment.