Decisions, Decisions

May 19, 2017

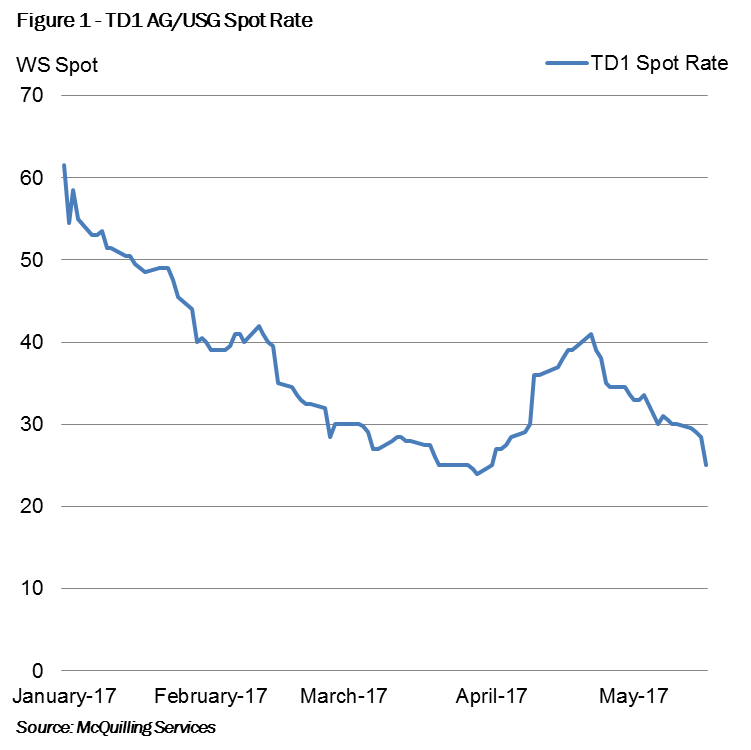

VLCC rates along the TD1 AG/US Gulf route dropped below WS 30 this week amid a weaker market structure (Figure 1). With overall cargo activity out of the Arabian Gulf stagnant over the past few months, we have seen pressure stemming from both the demand and supply sides of the equation.

Production cuts in the Middle East continue to push owners towards western markets in hopes of higher earnings, while those  that are left in the region must battle against disadvantaged tonnage fixing at lower levels. The decision of where to point the bow becomes increasingly tricky as owners must decide whether to take the chance on a long haul voyage West in hopes of fixing a backhaul trip at a decent rate to keep the ship occupied for the next 125-145 days or bite the bullet, remain in the region and take the shorter East voyage at weak time charter equivalent (TCE) levels with hopes that the market will recuperate in the near term.

that are left in the region must battle against disadvantaged tonnage fixing at lower levels. The decision of where to point the bow becomes increasingly tricky as owners must decide whether to take the chance on a long haul voyage West in hopes of fixing a backhaul trip at a decent rate to keep the ship occupied for the next 125-145 days or bite the bullet, remain in the region and take the shorter East voyage at weak time charter equivalent (TCE) levels with hopes that the market will recuperate in the near term.

While the earnings on cargoes loading in the West seem more attractive at the moment, our observations on tanker movements indicate that a larger percentage of VLCCs are ballasting directly to the West than in 2016. Additionally, the expectation of 34 more VLCCs to hit the water this year will add more pressure to earnings in this sector.

Going forward, we are closely monitoring the pending Organization of Petroleum Exporting Countries' (OPEC) decision. If, as reported, if the production cuts are extended, we see a stronger market for owners in the West on the basis of a tighter Brent/Dubai differential. Whereas the Arabian Gulf market would fare better if production cuts were discontinued, as Dubai pricing would likely become more attractive to Eastern buyers versus Atlantic Basin crudes. In our view the latter is more likely because even if cuts are extended, we forecast a much lower compliance rate than the first edition of the agreement.

Comments

You need to login to comment.