The Caribbean region has come under considerable pressure this year amid political uncertainty and depressed pricing for crude oil. Colombia, Mexico and Venezuela are the major producers in the region and currently account for about 4.6 million b/d of crude and condensate production, which compares to just below 4.9 million b/d in the beginning of 2017. All three nations have struggled from a lack of investment in the upstream sectors, which has been particularly tough since the oil price collapse of 2014.

What is the Tanker Market Outlook?

Dec. 21, 2017

Forecasting the future in most industries is an activity characterized by imprecise results. Nonetheless, firms must develop some basis for planning for their future business activities. This is especially true for those in the tanker shipping industry where marine logistics is a key part of the supply logistics chain and ships represent capital investments.

As Forties Falter, the US Moves In

Dec. 14, 2017

The Forties Pipeline System suffered a major shutdown this week after running at reduced rates since December 6 as a hairline crack in the 450,000 b/d pipeline near Red Moss in Aberdeenshire worsened. The system transports around 40% of UK North Sea oil production, connecting 85 fields to the British mainland and feeding Ineo’s refinery in Grangemouth. The shutdown is expected to last for several weeks as pipeline operator Ineos stated “no less than two weeks” and will likely push the current Forties loading program into the New Year. We note that Brent crude prices found immediate ...

Euro-zone Reaches New Highs

Dec. 12, 2017

Global manufacturing PMI reached its highest level since March 2011 this past month amid increased levels from nearly everywhere. One of the main drivers behind this growth has been the Euro-zone, which according to preliminary data reached its highest level since April 2000 at 60.1. While this data is based on preliminary estimates, we tend to believe the bullish trend as official monthly data from October indicates a surge in manufacturing activity. The manufacturing PMI of the Euro-zone has outpaced that of the US since the beginning of the year as European countries continue to hold the top eight ...

Pioneiro de Libra Leads the Pack

Dec. 8, 2017

The floating, production, storage and offloading unit (FPSO), Pioneiro de Libra, made headlines in November, kicking of the start of the Libra oilfield, the second to be developed in Brazil’s pre-salt area, with about 50,000 b/d of capacity. Additional crude supply is expected from the Lula and Campos fields with a 150,000 b/d FPSO and 30,000 b/d smaller project on track to begin in the first quarter of 2018. These new projects coupled with ramp-ups at the P66 150,000 b/d platform, additional crude production is expected to be 160,000 b ...

TC2 Runs Up

Nov. 30, 2017

Prior to the Thanksgiving holiday in the US, we expected that TC2 would find some freight rate support in the short-term as we moved into this week with a relatively thin tonnage list. This expectation has come to fruition over the last two days as TC2 opened to week at WS 125 and has risen to WS 160 as of today. This 35 WS point run-up is mainly driven by higher gasoline demand in West Africa pulling volumes out of the UKC and thinning the tonnage list in Northern Europe. With positions tight in the UKC and a relatively healthy ...

Filling the Gap: Part 3

Nov. 21, 2017

US crude has been making its way to Eastern markets in high volumes this year with official monthly data from the US Energy Information Administration (EIA) indicating an average of 896,000 b/d through August 2017. In the past, a majority of US crude was piped north into Canada; in fact, from 2010 to 2015 an average of 94% of US crude was exported to Canada. The removal of the ban on US crude exports at the tail end of 2015 allowed this figure to fall to 61% in 2016 amid higher flows to Northern Europe, the Caribbean, and ...

Filling the Gap: Part 2

Nov. 16, 2017

One major oil producing nation that we expect to fill the demand gap in the East is Brazil, which has increased crude production by 155,000 b/d year-on-year to 2.6 million b/d over the first 10 months of 2017. Levels are expected to rise further to upwards of 2.8 million b/d next year and with demand on track to rise to 1.78 million b/d, we foresee the crude balance available for export expanding by about 135,000 b/d on average next year. Export volumes into China continue to follow their upward trend ...

Filling the Gap: Part 1

Nov. 14, 2017

The Middle East and West Africa stand as two of the largest oil producing regions in the world accounting for over 32 million b/d of crude supply in 2017 and exporting 75% of that to refiners across the globe; however, their largest clients are located in Asia. Within Asia, the Far East and South East Asia regions currently account for around 29.3 million b/d of refining capacity; however, by 2025 this figure is on track to rise to over 32 million b/d. The outlook for regional crude supply is not as promising and expected to fall ...

The Orders Roll On

Nov. 9, 2017

Through the first 10 months of 2017, tanker contracting activity has increased relative to last year as through the same period of 2016 we recorded 109 vessels ordered, while this year we have seen 165 tankers place on order. Year-to-date, the bulk of ordering activity has been on the dirty side with 47 VLCCs, 18 Suezmaxes and 25 Aframaxes, while no Panamax newbuildings have been ordered. On the clean side, we have witnessed about 75 newbuilding contracts, 12 LR1s, 52 MR2s and 11 MR1s. Contracting activity still pales in comparison to 2015, when the market was booming and 267 vessels ...

Middle East Tensions Present Arbitrage Opportunities

Nov. 7, 2017

Tensions in the Middle East have surged recently as Saudi Arabia intercepted a missile launched out of Yemen, allegedly fired by Houthi rebels. According to the Saudi Press Agency, the missile was made in Iran and likely smuggled into Yemen, reinvigorating the belief that Iran has been arming Houthi rebels. Saudi Arabia has indicated that tensions may rise further as the Middle East power views the incident as an attack from Iran. This follows just a day after dozens of government, military and business officials were detained in an effort to combat corruption in Saudi Arabia. On the back of ...

Fleet Utilization

Oct. 18, 2017

Our analysis of remotely-sensed vessel position data captured only a small (+0.3%) rise in daily Suezmax demand in September versus August, but up 8.5% from the same month last year. Demand is projected to increase in October and November, likely placing some modest upward momentum in freight rates. Similar to the VLCC segment, a supply of tonnage has outpaced demand growth. As of the end of September, we calculated a 10.6% rise in Suezmax supply from year-ago levels, outpacing demand and reducing utilization to just 60.7% last month, the lowest rate since October 2015, highlighting the ...

McQuilling Forecast Performance

Oct. 12, 2017

Through the first nine months of 2017, our forecast performance when measured by the deviation from actual levels is tracking within 5.0% for the 12 DPP trades and 0.02% for the seven CPP trades in our Tanker Market Outlook. When compared to our front month forecasts from last month’s Short Term Outlook, we forecast September’s rates within 13% of actual market levels. Finally, in January, we project monthly rates given our proprietary model of seasonality behavior. For September, our January projections tracked within <0.1% of actual levels.

Politics and Pipelines

Oct. 10, 2017

Tensions in the Middle East have risen in recent weeks as the September 25 referendum in the Kurdistan region of Iraq received about 70% of registered voters and concluded with an overwhelming “yes” for independence. Immediately following the event, a curfew was established in Kirkuk and the Iraqi government considered sending troops into the area. While the use of military force has yet to be realized, Turkey is considering shutting Kurdish access to the pipeline to Ceyhan. The Kurdish Regional Government (KRG) stopped reporting its crude volumes; however, Iraqi volumes exported through the pipeline equated to about 550,000 b ...

Going Long on LR Tonnage

Sept. 28, 2017

Long-range product carriers operating in the Arabian Gulf region have enjoyed a recent run-up in rates as assessments for TC1 and TC5 have traded up 38% and 25%, respectively, since the start of September. In general, demand within this market has come under some pressure this year amid increased refining capacity in the East serving local demand as well as an extended maintenance schedule at refineries in the Middle East this year. Since late summer, maintenance levels have tapered off, redirecting cargo demand back to the market with a considerable jump in activity over September. Through September 28, we have ...

Crude Strength Will Be Short-Lived

Sept. 21, 2017

A steady flow of Northern European crude has been making its way to Asia this year as OPEC production cuts continue to boost pricing for Middle Eastern grades and push Eastern refiners to source barrels from the Atlantic Basin.

Mediterranean Crude Moves East

Sept. 19, 2017

The Mediterranean region continues to grow as a demand center for dirty tankers from a load perspective as the run up in regional crude supply has pressured pricing and increased arbitrage opportunities in a lower freight rate environment. Mediterranean crude supply is on track to rise by 460,000 b/d this year amid a recovery in Libyan and Kazakhstan production as well as redirected Russian barrels into the Black Sea.

What is Driving the US Export Growth?

Sept. 12, 2017

Since the former US administration lifted the ban on US crude exports at the conclusion of 2015, this market has experienced considerable growth within the global oil and gas industry. In 2016, US crude export volumes averaged about 591,000 b/d with a majority of the volumes to Canada and regional trading partners in the Caribbean. Some barrels were shipped to Northern Europe and the Far East; however, in relatively low quantities, when compared to levels witnessed today. Through the first half of 2017, we have observed US crude exports average at about 918,000 b/d with just ...

Hurricane Harvey Wreaks Havoc

Sept. 7, 2017

Hurricane Harvey broke the Texas coast on the night of Friday August 25 as a category four hurricane and within a day was downgraded to a tropical storm; however, massive rainfall placed the US’ fourth largest city under water. Record flooding has been reported throughout the Houston area, causing many oil majors to shut refinery operations. It is estimated that around 4-5 million b/d of primary distillation capacity was impacted with some operations returning quicker than others; however, the impact on 1.5 million b/d of capacity in the Port Arthur area has yet to be fully determined ...

Floating Storage Shifts

Aug. 29, 2017

As we noted in the 2017-2021 Tanker Market Outlook, an increasing amount of spot fixture activity has been carried out by disadvantaged tankers in 2017 as older tonnage tends to fix below market levels. Meanwhile, a notable amount of older tankers have been fixed for operational floating storage in the time charter market or optioned for short-term FSO duty in the spot market.

McQuilling Services’ Forecast Performance

Aug. 24, 2017

As part of our forecasting process, we like to evaluate our forecast performance throughout the year and provide our clients with the results (Figure 1). At the beginning of the year, we noted in our Tanker Market Outlook that the year 2017 is likely to be a down year for owners of all tanker classes on the basis of supply side risks. Similar to what we expected, over 180 tankers (DWT>27.5k) joined the trading fleet and our original forecasts for the 19 trades included in the 2017-2021 Tanker Market Outlook are only 3% above actual market levels for ...

Owners Continue to Order

Aug. 22, 2017

There have been 146 tanker orders placed through July, compared to just 56 during the same time period last year. The bulk of these orders have stemmed from the VLCC and MR2 classes as 39 and 47 firm orders have been placed, respectively (Figure 1). Maran Tankers placed a firm order for seven VLCCs at Daewoo this year, while BW/DHT has collectively placed six at Samsung and Hyundai Heavy Industries.

Global Product Demand and Supply at a Glance

Aug. 17, 2017

Global oil demand is expected to grow at 1.3% in 2017 to over 96.9 million b/d with significant gains projected in the middle-light end of the barrel. Over the forecast period (2017-2021), we are likely to see global oil demand expand by 1.0% annually, climbing above 100 million b/d. Among the biggest drivers of this growth are naphtha, gasoline and gasoil, with positive annual growth factors of 1.5%, 2.1% and 2.0%, respectively (Figure 1). On a regional basis, emerging economies in the Far East and South East Asia are expected to boost ...

OPEC Efforts are Counteracted

Aug. 15, 2017

In 2016, OPEC members established a concerted effort to rebalance the global oil market through production cuts, which would be implemented by all members excluding Iran, Libya and Nigeria. After implementing the agreement on January 1, 2017, total crude output from the group over the first half of 2017 has fallen by 400,000 b/d year-on-year; however, when compared to 2016’s full year average, we see a greater decline of over 800,000 b/d.

McQuilling Services Announces the Release of the 2017 Mid-Year Tanker Market Outlook Update

Aug. 9, 2017

McQuilling Services is pleased to announce the release of the Mid-Year Tanker Market Outlook Update. The Mid-Year Tanker Market Outlook Update provides an outlook for monthly spot market freight rates and TCE revenues for 19 major tanker trades across eight vessel segments for the second half of 2017 and the remaining four years of the forecast period.

McQuilling Services 2017-2021 Mid-Year Tanker Market Outlook Update

Aug. 1, 2017

McQuilling Services is in the midst of producing its 20th Anniversary Edition 2017-2021 Mid-Year Tanker Market Outlook Update and is proud to announce its release the week of August 7th, 2017. The Mid-Year Tanker Market Outlook Update provides an outlook for spot market freight rates and TCE revenues for 19 major tanker trades, including two triangulated trades, across eight vessel classes for the second half of 2017 and the remaining four years of the forecast period to 2021.

A Temporary Tumble

July 20, 2017

Suezmax fixing activity in the Black Sea has increased considerably this year largely due to higher production in Kazakhstan pushing barrels through the Caspian Pipeline Consortium (CPC) to Novorossiysk. Kazakhstan crude and condensate output has risen to over 1.7 million b/d in recent months, underpinned by a ramp up of operations at the massive Kashagan oilfield.

Pressure Mounts

July 18, 2017

VLCC voyages from the Middle East to North America continue to decline this year, falling below 2016 levels and reducing TD1 earnings as pressure mounts from both sides of tanker fundamentals. On the supply side, OPEC’s efforts to rebalance global oil benchmarks has led to a reduction in Middle East crude volumes to the West as producers battle to retain market share in the East. From the demand side, rising crude supply in North America due to steady production gains in Canada and the US has reduced the reliance on imports from the Middle East. Vessels along this route ...

Taking Advantage of McQuilling.com

July 11, 2017

McQuilling’s website strives to provide users with the necessary tools and information within the company’s broad maritime expertise in order to assist individuals through our six main website sections: About, Products & Services, Industry Tools, Locations, News Headlines, Blog, and McQuilling TV. Each section has a specific ability to assist users, although premium content features are only accessible by registering on our website. Registration is completely free, and the majority of our premium content is complementary to our registered users. We suggest that all users create an account in order to access our company’s premium content, as well ...

Rate Rally in the Gulf

June 27, 2017

Freight rates for clean tankers in the US Gulf-Caribbean are on the rise, underpinned by a conglomerate of supportive fundamentals. TC3 was assessed at WS 195 today, a 26% rise from June’s open, while freight on the US Gulf > Carib route has risen by US $150,000 over the same period. US Gulf refiners continue to run at high utilization with crude intake reaching 17.2 million b/d in the last week, boosting gasoline inventories to 242 million barrels. Clean cargoes out of this region have been plentiful with total US product exports averaging at 5.1 million ...

After the Expansion

June 15, 2017

Utilizing our remotely sensed vessel position data, we took a look into the aftermath of the Panama Canal Expansion project. Our data shows that the monthly average of Panama Canal tanker transits reached 85 trips in the first five months of 2017, a 16.5% year-on-year increase from 2016. The passage way concluded its expansion in June of 2016, which added a third set of locks and doubled the canal’s transit capacity. Since the beginning of 2017, we have seen a notable rise in Aframax/LR2 sized transits following a lack of activity in the second half of 2016 ...

Weekly Tanker Market Snapshot

June 9, 2017

The following is an overview of tanker spot market activity for the week ending June 9, 2017

VLCC

We counted about 20-22 vessels reported fixed or on subjects in the Arabian Gulf this week with freight rates relatively steady at WS 50 for AG/East depending on factors such as age, preferred destination and if the vessel was disadvantaged. The TCE for a voyage on the AG/Japan route was pegged around US $16,000/day (WS 50), while AG/West paid in the mid to high WS 20s with less downward due to the fact that the follow up ...

The Perfect Storm

June 7, 2017

Suezmax freight rates out of West Africa have come under recent pressure, plagued by poor fundamentals on both the demand and supply sides of the equation in what can be described as “the perfect storm.” Despite reports of higher crude output in Nigeria and the recent lifting of force majeure on the Forcados crude stream, we have observed just five vessels reported fixed or on subjects by mid-week, representing softer tanker demand. From a vessel supply perspective, the tonnage list in West Africa remains long, compounded by a weaker Arabian Gulf market sending ballasters into the region.

With the tonnage ...

Shuttle Tanker Snapshot

May 25, 2017

A shuttle tanker is a vessel specifically designed to transport oil from offshore oil fields or large oil tankers to onshore refineries. While this is typically the function of a pipeline, a shuttle tanker may be preferred due to their flexibility to transport oil to any destination, easy maintenance and ability to safely operate in harsh climates and deep water regions. Shuttle tankers are equipped with computerized technology, known as “dynamic positioning,” which help to keep the vessel on position at all times. They also offer additional benefits that pipelines cannot, including the ability to segregate oil, while pipelines usually ...

Intertanko Annual Tanker Event 2017

May 22, 2017

On Thursday, May 25, McQuilling Services' Senior Shipping and Finance Advisor, Stefanos Kazantzis, will participate in the "Role of the Broker" Panel Discussion at Intertanko's Annual Tanker Event 2017. The panel discussion will commence at 1400 hours in the Grande Ballroom at the Houstonian Hotel and will aim to cover the following topics:

Brokers - forecasters or fixers?

Is the role of the broker evolving in step with the changing face of the chartering and S&P sector and the changing roles of the individual players?

Impact of technology on the interaction between industry participants

Broker projects desks add strategic ...

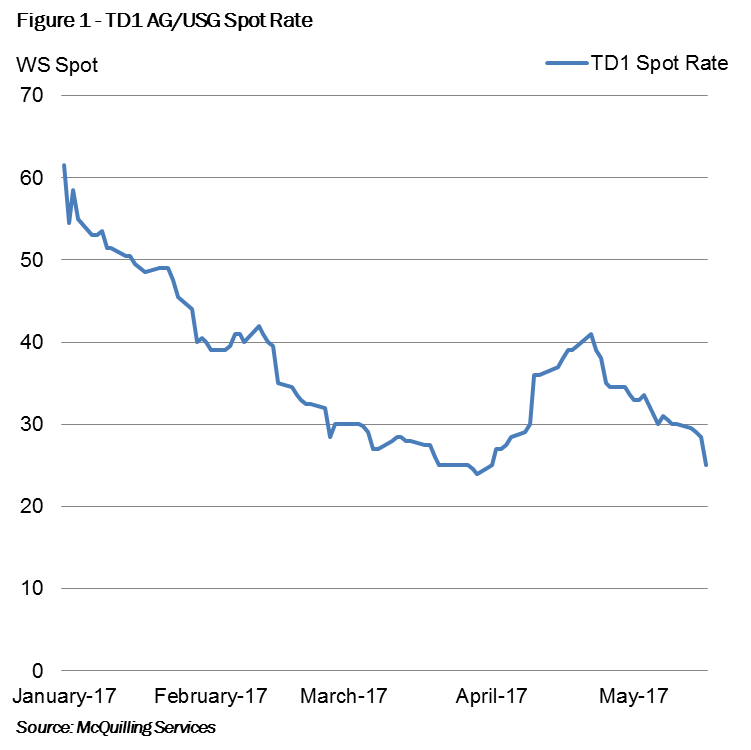

Decisions, Decisions

May 19, 2017

VLCC rates along the TD1 AG/US Gulf route dropped below WS 30 this week amid a weaker market structure (Figure 1). With overall cargo activity out of the Arabian Gulf stagnant over the past few months, we have seen pressure stemming from both the demand and supply sides of the equation.

Production cuts in the Middle East continue to push owners towards western markets in hopes of higher earnings, while those that are left in the region must battle against disadvantaged tonnage fixing at lower levels. The decision of where to point the bow becomes increasingly tricky as owners ...

McQuilling to Present at MarineLog's Tugs & Barges Conference

May 15, 2017

We are pleased to announce McQuilling Services' Senior Shipping and Finance Advisor, Stefanos Kazantzis, will be giving a presentation on the "Near Term Outlook for Tankers" at MarineLog's 14th Annual Tugs and Barges Conference on May 16 at 11:30am. The two-day event will be held at the Stamford Marriot Hotel in Stamford, CT.

The presentation will cover the following topics:

Oil Supply and Demand

Tanker Demand

Tanker Supply

Tanker Market Outlook

A copy of the "Near Term Outlook for Tankers" will be available on mcquilling.com on Wednesday, May 17.

Weekly Tanker Market Snapshot

May 12, 2017

The following is an overview of tanker spot market activity for the week ending May 12, 2017

VLCC

Activity in the Arabian Gulf fell off this week with around 17-18 vessels reported fixed or on subjects, while the monthly figure for May stands at about 123-124 ships. We estimate the TCE for TD3 followed by a Caribbean/Singapore voyage is down about $5,500/day to $32,500/day. TD3 was estimated steady at about US $21,000/day for modern tonnage, while disadvantaged tonnage was fixing at a discount. In the Atlantic Basin market, we counted around 3-4 ships ...

2020 Bunker Regulation - "A Refined View"

March 23, 2017

Over the next five-year period, the regulatory environment of marine transportation will adapt according to new environmental policies. Two monumental changes in maritime operations are fast approaching, one being the global 0.5% Sulphur Emissions Cap, which will begin in 2020 as a way to reduce the carbon footprint created by maritime transportation.

JBC Energy, a boutique oil market research company based in Vienna, has recently released a multi-client studythat tackles the IMO regulatory change from every relevant angle, providing a detailed take on the supply, demand and price changes that have to be expected in the wake of ...

What's in Store for Tanker Supply?

March 8, 2017

Tanker tonnage supply has been a topic of interest recently, with many market participants eager to know when the fleet may experience a slim down. Vessel exits have been limited over the past few years, falling to a low of less than 30 in 2015. This slowdown has occurred during a time when the pace of newbuilding deliveries has been elevated, averaging 230 new ships per year since 2010. This imbalance has caused the global fleet count to swell to over 4,700 ships in 2017, up 28% from 2010.

The question now is, will there be an increase in ...

McQuilling Services Announces Release of 2017-2021 Tanker Market Outlook

Jan. 25, 2017

New York – January 25, 2017 – McQuilling Services is pleased to announce the release of its 20th Anniversary Edition 2017-2021 Tanker Market Outlook. This 200-page report provides a five-year spot and time charter equivalent (TCE) outlook for eight vessel classes across 19 benchmark tanker trades, plus two triangulated trades. Also included in the report is a robust five-year asset price outlook as well as a one and three-year time charter forecast through 2021.

With 20 years of tanker rate forecasting expertise, McQuilling Services is a leader in the industry and continues to support a variety of stakeholders in the energy ...

McQuilling Services' Outlook Methodology

Jan. 17, 2017

Over the past 20 forecasting cycles, the primary objective of producing the Tanker Market Outlook has been to develop a logical thought progression based on demand and supply fundamentals for our clients’ use. Our industry models are intended to explain a significant portion of the behavior of tanker spot freight market levels and to project them into the future. While the concepts remain quite intuitive, the math has become increasingly complex.

McQuilling Services uses a multi-dimensional approach for producing forecasts which combines analysis with experience and observation. The resulting forecasts are based on a combination of results from analytical regression ...

What is the Tanker Market Outlook?

Jan. 9, 2017

Forecasting the future in most industries is an activity characterized by imprecise results. Nonetheless, firms must develop some basis for planning for their future business activities. This is especially true for those in the tanker shipping industry where marine logistics is a key part of the supply logistics chain and ships represent capital investments.

Twenty forecasting cycles ago, marine transport consultancy, McQuilling Services, recognized a need for tanker freight rate forecasts, which is why they developed what’s known today as the “Tanker Market Outlook.” This report, produced on an annual basis, provides market participants with a five-year tanker freight ...

With the tonnage ...

With the tonnage ... that are left in the region must battle against disadvantaged tonnage fixing at lower levels. The decision of where to point the bow becomes increasingly tricky as owners ...

that are left in the region must battle against disadvantaged tonnage fixing at lower levels. The decision of where to point the bow becomes increasingly tricky as owners ...