")

602, 2026

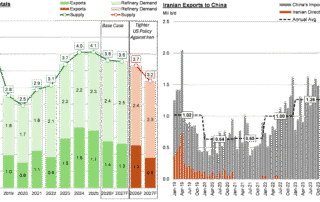

Maximum Pressure on Iran Oil Flows

Iran’s crude fundamentals have been heavily impacted by the US [...]

2301, 2026

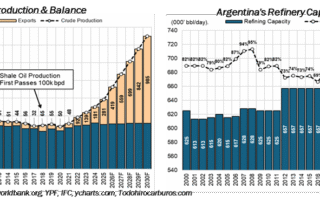

Argentina A New Potential LATAM Player

Until recently, Argentina’s crude oil production peaked in May 1998 [...]

1601, 2026

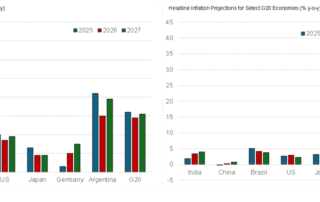

Global Economic Update

Over the past month, major world economies have continued to [...]

901, 2026

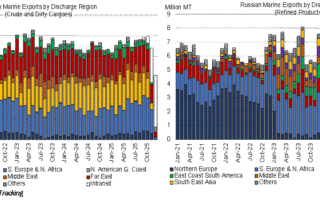

2025 Russian Crude & CPP Exports

Despite the latest US penalties on Rosneft and Lukoil and [...]

1912, 2025

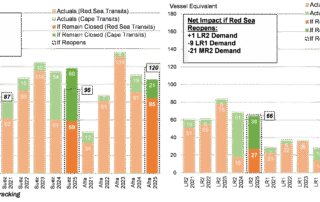

Red Sea Reopening Scenario

The change in trade flows and market fundamentals so far [...]

1212, 2025

US Sanctions on Russian Oil and a Potential Peace Deal

The US government jolted energy markets when it announced sanctions [...]