McQuilling Services latest industry note, Naphtha Exiting the European Union, was co-authored by JBC Energy, a leading research institute that offers independent and unbiased expertise for the global energy sector from Vienna, Austria. This note aims to provide the tanker industry with unique insight into the outlook for West to East naphtha tanker flows in the second half of 2016 and the impact on corresponding clean tanker rates.

Weekly Tanker Summary

June 24, 2016

The following is an overview of tanker spot market activity for the week ending June 24, 2016.

VLCC

There was an uptick in AG activity week-on-week and a demand spike mid-week helped to absorb a lot of excess tonnage from June and the first 10 days of July. AG/East rates bottomed at WS 36-38 before bouncing back to the WS 45 level by week’s end. Rates for AG/West traded steady in the mid-WS 20s for the majority of the week and then moved up into the high WS 20s before close.

There was also an increase in ...

McQuilling Services Presents at Intertanko

June 23, 2016

On May 25, 2016, the Director of McQuilling Services Singapore, Ms. Katharine Cheong-Koh, gave a presentation on the Global Chemical Tanker Outlook at the 2016 Intertanko Annual General Meeting in Capella Sentosa in Singapore. The presentation focused on evolving chemical tanker trading lanes, the regional competitive landscape and identified investment opportunities for this sector over the next few years.

For a selection of key takeaways from the presentation, please contact katharine.c.koh@mcquilling.com.

The Benefits of Registering on McQuilling.com

June 21, 2016

Whether you are an owner, charterer, operator or investment banker, there are many benefits to becoming a registered user on McQuilling.com. Besides being completely complimentary, registration gives users access to premium content on the site, which is outlined below:

Industry Notes

Industry-leading analysis from research and consulting firm, McQuilling Services, on trending market topics. These notes are published on a bi-monthly basis and provide readers with in-depth insight on factors influencing the global shipping markets.

Tanker Podcasts

Stay on top of what’s driving the tanker markets with a weekly 5-minute overview of spot and period market activity ...

Weekly Tanker Summary

June 17, 2016

The following is an overview of tanker spot market activity for the week ending June 17, 2016

VLCC

Volume in the AG fell week-on-week and rates for AG/East declined to the high WS 30s, down over 20 WS points from the close of the previous week, while AG/West dipped into the mid-WS 20s. On the other hand, activity picked up in the Atlantic Basin as 13-14 fixtures were reported. Despite the uptick, WAFR/China rates fell to the low WS 50s, while an East Med/UKC cargo was concluded at WS 50. In the Western Hemisphere it was ...

Monthly Tanker Update: May

June 16, 2016

Crude oil production has come under pressure in several countries, specifically West Africa as a surge in militant attacks has reduced Nigeria’s output by about one million barrels per day. The lost production in Nigeria has helped to support crude prices which have climbed to above $50 per barrel for the first time since November 2015. Prices have also found further support from outages in Canada stemming from wildfires in the oil sands region as well as Venezuela and Libya.

The United States has also seen a reduction in domestic crude oil production as it fell to an average ...

Venezuela Port Delays

June 15, 2016

Venezuela’s economy has been on a downward spiral since the collapse of global crude oil prices and the situation appears to be getting worse for the oil-dependent country as production dropped to 2.37 million b/d in May, down 10.7% from the full year average for 2015 (according to data published by OPEC).

Because of its continued economic hardship, cash-strapped Venezuela has been challenged to pay oil suppliers, delaying tankers from loading and unloading cargoes on time. Our analysis of AIS position data has showed a rising number of DPP tankers (27,000 dwt and above) either ...

Weekly Tanker Summary

June 10, 2016

The following is an overview of tanker spot market activity for the week ending June 10, 2016.

VLCC

Activity remained steady week-on-week in the Arabian Gulf. AG/East rates rose back into the high WS 60s, with some spikes into the low WS 70s. Rates to the West traded steady at an average of WS 35. In the Atlantic Basin, WAFR/China rates remained steady in the mid-WS 60s.

SUEZMAX

Volume fell again in West Africa and rates initially held last week’s closing levels as WS 82.5 was achieved early on, but this was short-lived as a cargo ...

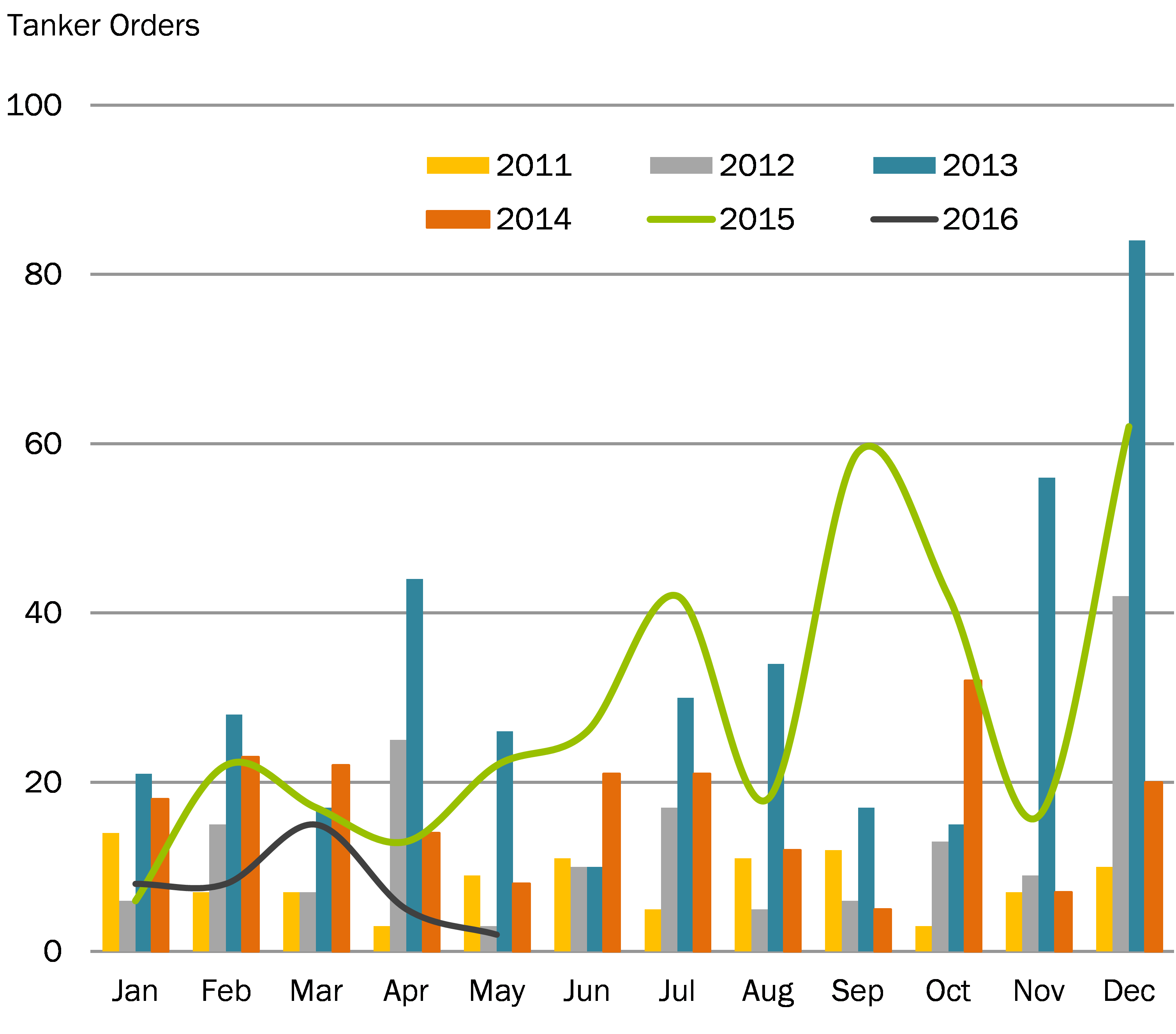

The Tanker Orderbook

June 7, 2016

Nearly half of the year is behind us and one thing that continues to stand out is the lack of a tanker newbuilding orderbook. We have recorded just 38 orders placed through May. The last time we saw activity this low was in 2011, when 40 newbuilding orders were recorded during this same period.

Leading the year’s orders so far is the Suezmax class, with 10 in the books, followed by the MR2 class with nine orders. Third in line is the Aframax class, accounting for 19% of the total 2016 orderbook. Absent from the list so far ...

Weekly Tanker Summary

June 3, 2016

The following is an overview of tanker spot market activity for the week ending June 3, 2016.

VLCC

Activity levels continued to climb in the Arabian Gulf and AG/East rates slowly rose back into the mid-to-high WS 60s, while AG/West paid in the mid-WS 30s. We are now heading into the third decade of June with 90 vessels fixed so far for the month and we would expect to see another 30-35 ships fix before the June program comes to a close. In the Atlantic Basin, WAFR/China increased slightly to the mid-WS 60s, up from the high ...

ist so far ...

ist so far ...