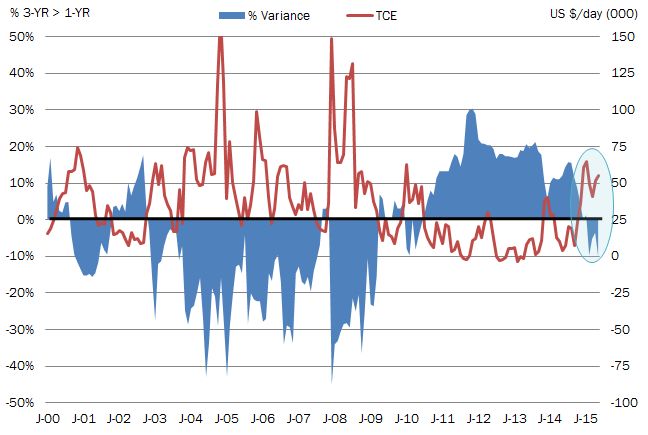

Among the many questions facing the tanker markets today, none stands out more than whether this recent rally in rates is a long-term cyclical shift or little more than a head fake? While not all sectors of the tanker market will trend in the same direction, we note a recent development that may provide some clues about the direction of the crude tanker markets. For the first time in 55 months, the 1-year time charter rate for the VLCC and Suezmax sectors has risen to a level greater than that of the 3-year time charter rate (Figure below).

In May ...

Dirty Tanker Supply at a Glance: May 2015

May 28, 2015

In the 2015-2019 Tanker Market Outlook published in January, McQuilling Services projected that 67 crude newbuildings would deliver to the trading fleet, while 31 dirty ships would exit the fleet via demolition or conversion in 2015. Based on this forecast, we would have expected that through May, 28 ships would have delivered to the trading fleet and 13 would have been sold for demolition or conversion.

Actual figures show that deliveries are lagging behind our initial forecast as 20 ships have been delivered, compared to our year-to-date expectation of 28. Exit activity is also slightly behind our year-to-date expectation of ...

Tanker Market Commentary

May 20, 2015

Clean East | LRs in the AG are slowly beginning to see higher rates - hearing TC1 was fixed at WS 104 and TC5 on subs for WS 125. The tonnage list is still tight for the first decade of June; however, the MRs in that region are still soft. The south is tight and rates are firming with WS 185 seen for a Spore/Oz voyage. The North is slowing down and rates are falling.

Panama Canal Expansion

May 14, 2015

Suezmax cargoes originating in the Caribbean (Colombia, Venezuela) with discharge in the Far East are examples of candidates for transiting the Panama Canal; however, key considerations including loadable quantity restrictions and Panama Canal costs will likely offset the benefit from the shortening of distances using current East-bound routing options for these trades.

In McQuilling Services most recent industry note, we evaluate the voyage economics pertaining to these trades for the year 2016. The basis of our analysis will be the calculation of the cost per barrel for loadings transiting through the canal compared to those routing through the open-seas.