More US Crude to Come

Oct. 17, 2018

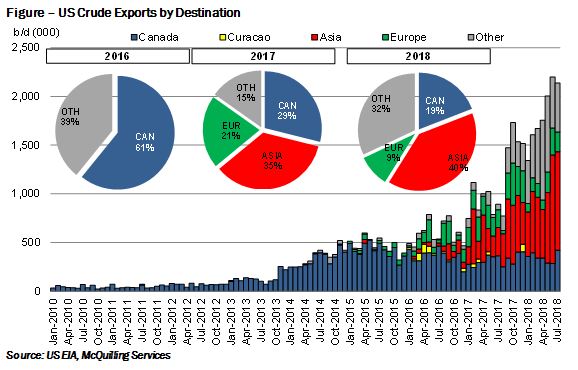

The latest US Energy Information Administration (EIA) official monthly shows the continued strength in US crude production with July up to 10.96 million b/d, a gain of roughly 270,000 b/d month-on-month. This also marked one of the higher months for crude exports with 2.1 million b/d observed in July, compared to 2.2 million b/d in June. Since this period, volumes have declined considerably amid a narrowing of the Brent-WTI crude differential, which averaged just US $3.27/bbl over July compared to US $6.85/bbl in the prior month. The lower pricing spread provides less incentive to ship larger stems to the East and instead promotes more intra-regional trading within the Atlantic Basin. This coincided with increased trade tensions between the US and China, the largest purchaser of US crude oil, and resulted in a complete halt to volumes. Through the first seven months of 2018, Asia remained the largest importer of US crude with 40% of the volumes amid higher volumes to Korea, India, China and Japan (Figure). The majority of the growth is attributed to China; however in recent months activity has shifted to other countries.

According to weekly estimates from the EIA, US crude exports have averaged 1.8 million b/d since the conclusion of July. Our fixture data for VLCC and Suezmax activity indicates that 24% of the volumes fixed to load July-September are bound for destinations West of the Suez, compared with a figure of 21% observed for January-June loadings supported by the narrower, Brent-WTI differential. During this period we also note an increase in share of activity served by Suezmax tonnage at the expense of VLCCs, supporting our notion that intra-regional trading is more supportive of tonnage below the VLCC size. October represents a reversal of both these trends with volumes booked to the West back down to 15%, while only 31% of the activity was served by Suezmax tonnage, compared to an average of 59% the three months prior. We expect this trend to continue going forward, as the wider Brent-WTI differential promotes more long-haul activity to the East on larger tonnage. However, with the lack of interest from China, we expect the focus of volumes to Korea, India and Japan.

Comments

You need to login to comment.