Suezmaxes Find Utilization Support

June 19, 2018

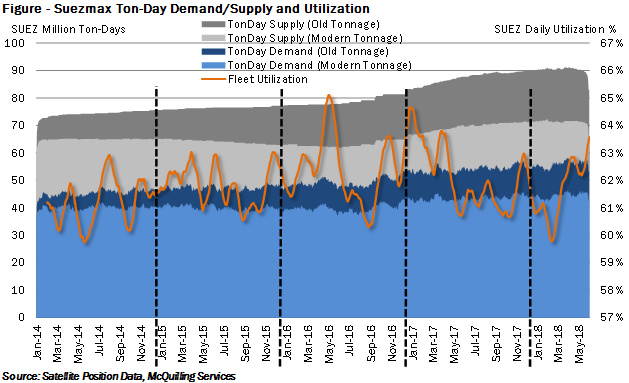

Throughout May, we observed Suezmax freight rates make considerable gains compared to the previous month with TD6 trading up about 16% month-on-month. Gains along this trade as well as others can be attributed to 63.4% utilization in May versus 62.1% the prior month (Figure). This is driven by stronger demand fundamentals against vessel supply (which declined month-on-month) as the Black Sea/Mediterranean market continues to provide support for this sector. We count roughly 124 loadings in this region in May, a 65% gain month-on-month and the highest levels since 2014, when our vessel position data begins. Spot fixing activity from CPC gained considerably in May as a lack of Aframax tonnage resulted in charterers booking Suezmaxes for the smaller stems. Through the first half of June, utilization has remained elevated at 63.2%, keeping most rates above prior month levels.

From the supply side, Suezmax ton-day supply rose 4.2% year-on-year, the lowest gain we have witnessed year-to-date and just 3.2% above January levels at 89 million tons (Figure). For May, this represents about 576 Suezmaxes as compared to the year-to-date average of 580 Suezmaxes, indicating weakness from the supply side of the equation. We count 20 Suezmax tankers left to deliver in 2018, which will bring full year net fleet growth to 28 vessels and keep a cap on any major rate gains. Going forward, rising refinery demand in Europe is likely to keep this vessel class busy, especially from the Mediterranean and West Africa; however, we may begin to see some short-term pressure on AG>Mediterranean activity amid uncertainty surrounding Iranian sanctions. Middle East volumes to the Indian Sub-Continent are gaining this year and a simple extrapolation for the remainder of 2018 indicates that Suezmax volumes could rise 27% year-on-year, although pressure on Iran could negatively impact this trend.

Comments

You need to login to comment.