The Return of Brazilian Demand

Oct. 10, 2018

The Brazilian economy is on track to expand by 1.8% this year, a downward revision from the International Monetary Fund’s (IMF) initial expectation of 2.3% in January. This downward revision is due to lower than expected consumption, exacerbated by fuel strikes observed across the country, placing a halt on the transportation of goods. As a result, refined product demand found pressure in May, particularly for gasoline and diesel with the former finding additional weakness in a preference for ethanol consumption due to higher fuel pricing. We are beginning to see demand pick up yet again; however, a lack of growth in refinery intake coupled with outages has resulted in higher import activity. The Replan refinery experienced a fire in August, causing the shutdown of 415,000 b/d of crude processing capacity. The refinery has resumed partial operations, but is not expected to become fully operational until next month. This coupled with a return of domestic demand has increased import requirements over the last few months.

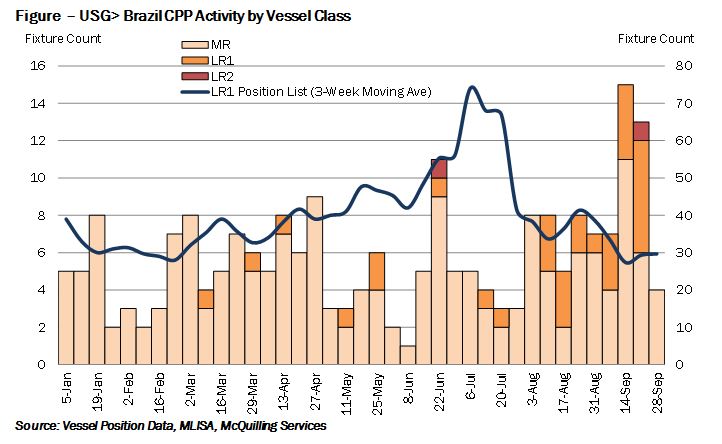

One source for this import stream is the US Gulf, which is typically served by MR2 tonnage; however, we have since observed an increasing presence of LR1 tonnage along this route. Looking at our propriety fixture data, out of the total volume fixed from the US Gulf to Brazil, the first two months of 2018 observed 100% MR activity; however, this began to face pressure in March, down to 96%. The MR market share slowly declined over the following months, falling to its lower level in August, just 74%, while 26% was served by LR1 tonnage. For September, a similar trend was observed with 64% of the activity LR1 tonnage, 3% LR2 tonnage and 33% MR tonnage. As noted in the Figure below, the preference for larger tonnage was largely driven by increased availability of LR1s. We observed the LR1 US Gulf position rise to a three-week moving average of 74 vessels in the beginning of July, likely placing some pressure on rates for these vessels relative to MR tonnage. For now; however, the tonnage list has been reduced and with the recent build-up of gasoline stock in the US to 235 million barrels, well above the five-year average for this time period, we expect more activity to the Caribbean and South America. Specifically, more volumes are likely to be sent to Brazil in the context of rising product demand in the final quarter of 2018.

Comments

You need to login to comment.